Tax Transcript Decoder©

COMPARISON OF 2018 TAX RETURN AND TAX TRANSCRIPT DATA

2020-21 Award Year (Version 1.0)

© 2019 NASFAA. All rights reserved.

Information in this publication is current as of October 31, 2019.

© 2019 by National Association of Student Financial Aid Administrators (NASFAA). All rights reserved.

NASFAA has prepared this document for use only by personnel, licensees, and members. The information contained herein is protected by copyright.

No part of this document may be reproduced, translated, or transmitted in any form or by any means, electronically or mechanically, without prior written

permission from NASFAA.

NASFAA SHALL NOT BE LIABLE FOR TECHNICAL OR EDITORIAL ERRORS OR OMISSIONS CONTAINED HEREIN; NOR FOR INCIDENTAL OR

CONSEQUENTIAL DAMAGES RESULTING FROM THE FURNISHING, PERFORMANCE, OR USE OF THIS MATERIAL.

This publication contains material related to the federal student aid programs under Title IV of the Higher Education Act and/or Title VII or Title VIII of the

Public Health Service Act. While we believe that the information contained herein is accurate and factual, this publication has not been reviewed or

approved by the U.S. Department of Education, the Department of Health and Human Services, or the Department of the Interior.

The Free Application for Federal Student Aid (FAFSA

®

) is a registered trademark of the U.S. Department of Education.

NASFAA reserves the right to revise this document and/or change product features or specifications without advance notice.

November 2019

2

Tax Transcript Decoder©

Comparison of 2018 Tax Return and Tax Transcript Data

FAFSA instructions direct applicants to obtain information from certain lines on IRS income tax returns and schedules. For

the most part, the instructions identify the relevant lines on the tax form by line number. These line item numbers do not

appear on IRS tax transcripts. Instead, each item is identified by name. When verifying FAFSA data using tax transcripts, it is

important to identify the correct answer.

The following pages contain a sample tax return and corresponding tax return transcript. Relevant line items have been

highlighted as follows:

Red: information to help cross-reference tax return line items with corresponding data on the tax return transcript.

Yellow: tax return line items that are required verification data elements for the 2020-21 award year.

Blue: tax return line items listed in the FAFSA instructions, which should be reviewed for potential conflicting information.

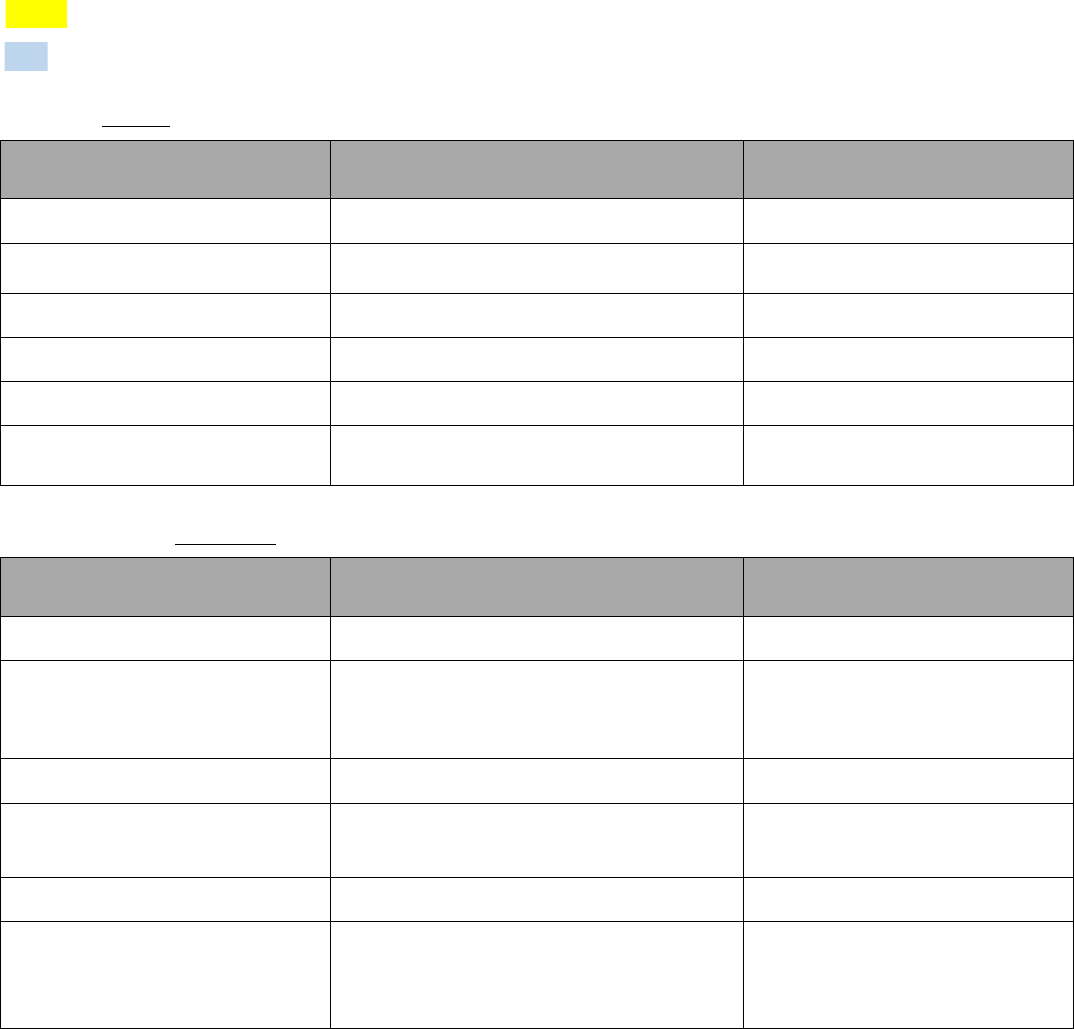

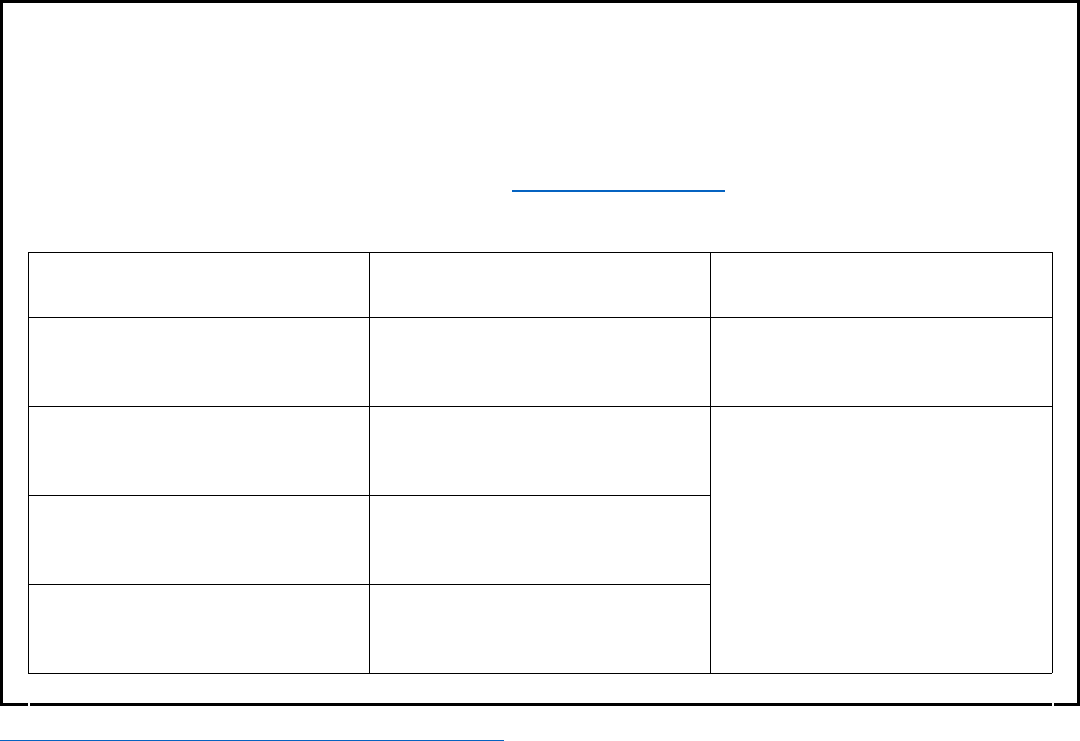

2018 Tax Return Line Items for 2020-21 Verification

1040 and Schedules

2020-21

FAFSA Question

AGI 1040 Line 7 36 (S) and 84 (P)

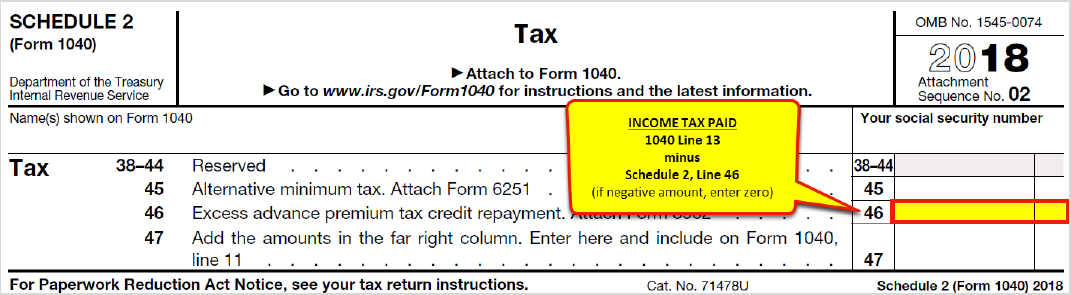

Income tax paid*

1040 Line 13 minus

1040 Schedule 2, Line 46

37 (S) and 85 (P)

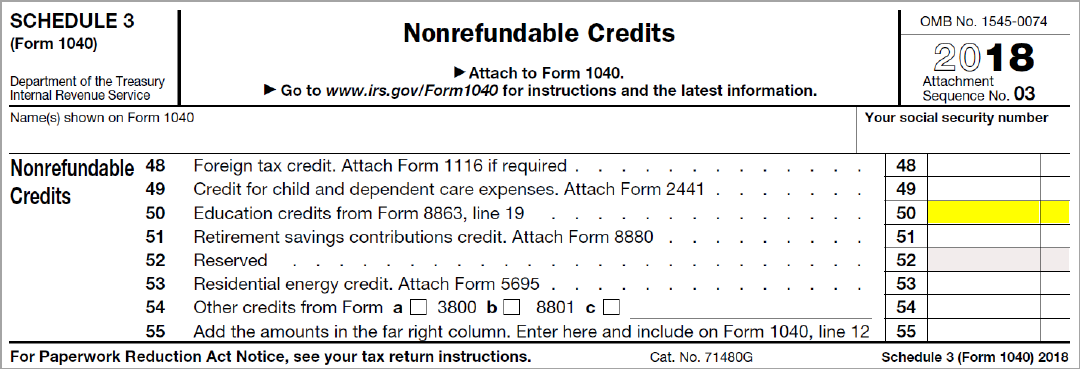

Education credits 1040 Schedule 3, Line 50 43a (S) and 91a (P)

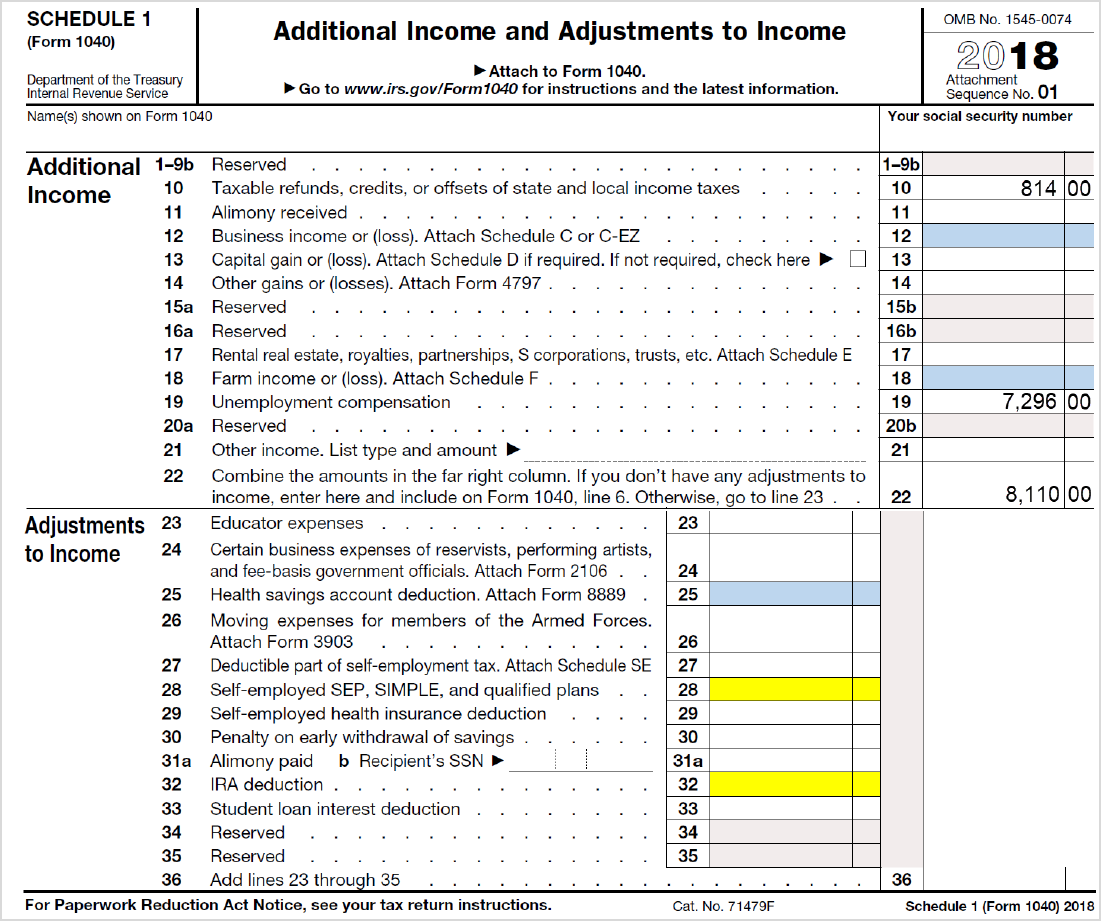

IRA deductions and payments 1040 Schedule 1, Line 28 + Line 32 44b (S) and 92b (P)

Tax-exempt interest income 1040 Line 2a 44d (S) and 92d (P)

Untaxed portions of IRA, pension, and

annuity distributions (withdrawals)*

1040 Line 4a minus 4b

(exclude rollovers)

44e (S) and 92e (P)

2018 Tax Return Transcript Line Items for 2021-21 Verification

Tax Transcript

2020-21

FAFSA Question

AGI “ADJUSTED GROSS INCOME PER COMPUTER” 36 (S) and 84 (P)

Income tax paid*

“INCOME TAX AFTER CREDITS PER COMPUTER”

minus

“EXCESS ADVANCE PREMIUM TAX CREDIT

REPAYMENT AMOUNT”

37 (S) and 85 (P)

Education credits “EDUCATION CREDIT PER COMPUTER” 43a (S) and 91a (P)

IRA deductions and payments

“KEOGH/SEP CONTRIBUTION DEDUCTION”

plus

“IRA DEDUCTION PER COMPUTER”

44b (S) and 92b (P)

Tax-exempt interest income “TAX-EXEMPT INTEREST” 44d (S) and 92d (P)

Untaxed portions of IRA, pension, and

annuity distributions (withdrawals)*

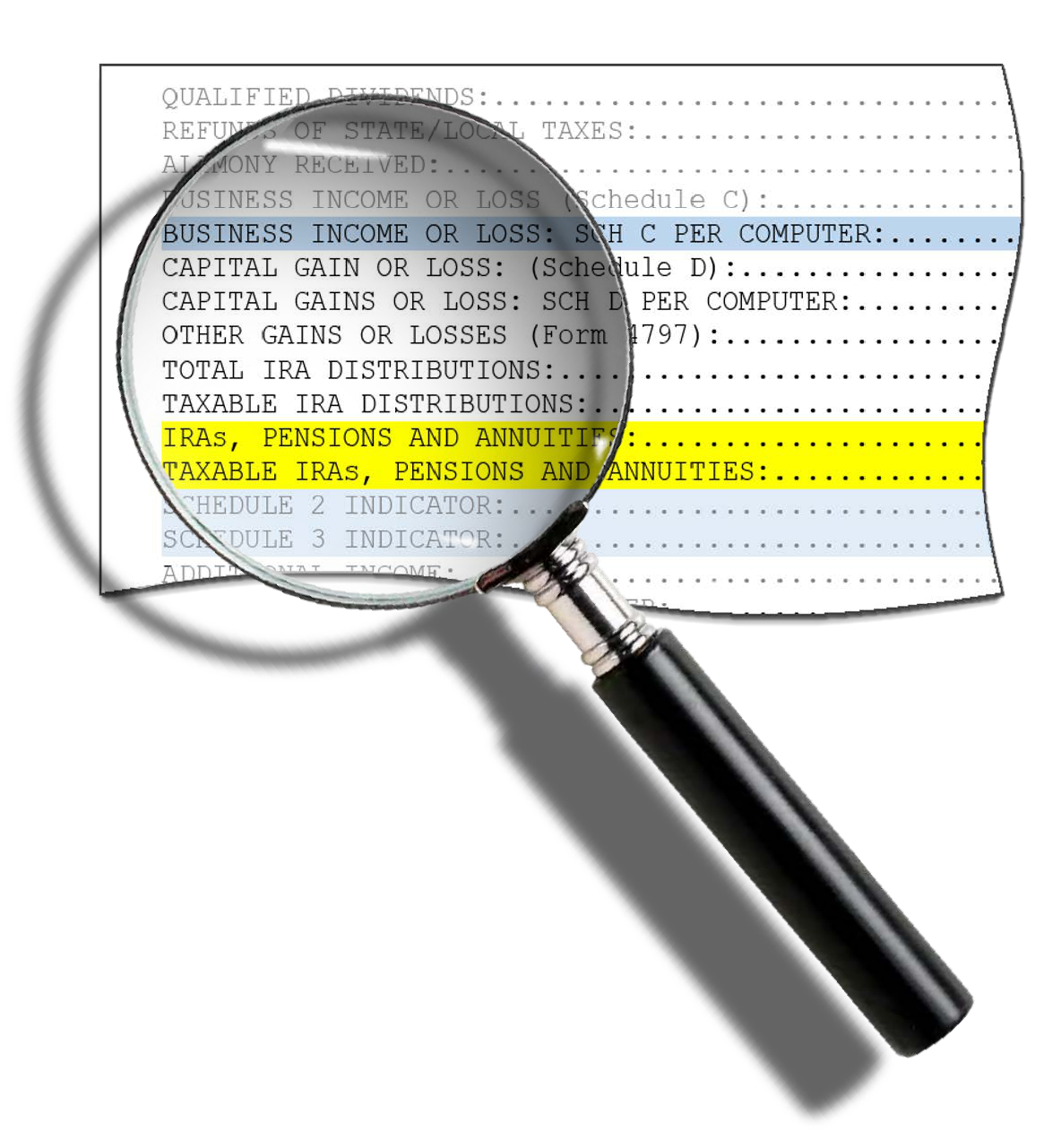

“IRAs, PENSIONS AND ANNUITIES”

minus

“TAXABLE IRAs, PENSIONS AND ANNUITIES”**

(exclude rollovers)

44e (S) and 92e (P)

*If negative, enter zero.

**The U.S. Department of Education (ED) is still awaiting IRS confirmation of the Tax Return Transcript line items for “TAXABLE IRAs, PENSIONS

AND ANNUITIES.”

3

© 2019

NASFAA. All rights reserved.

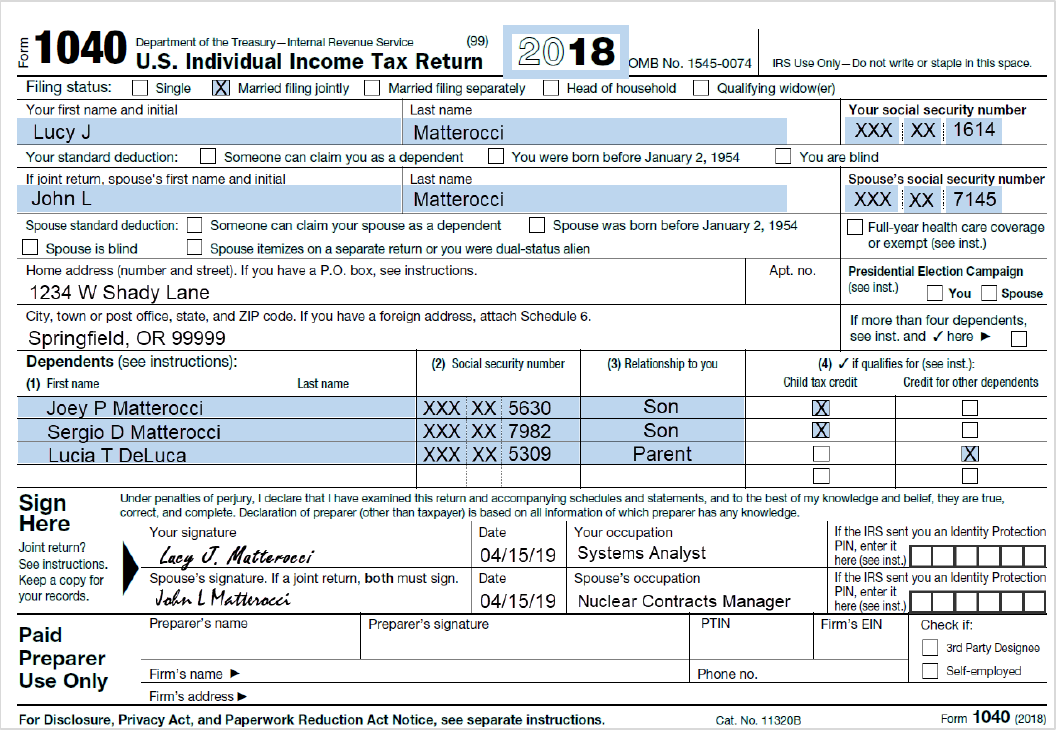

Sample IRS Form 1040, Page 1: Lucy and John Matterocci

4

© 2019

NASFAA. All rights reserved.

Sample IRS Form 1040, Page 2: Lucy and John Matterocci

*Income earned from work: IRS Form 1040--Line 1 , Schedule 1--Lines 12 and 18 , Schedule K-1 (IRS Form 1065)--Box 14 (Code A). If any individual earning item is

negative, do not include that item in your calculation.

5

© 2019

NASFAA. All rights reserved.

Sample IRS Form 1040 Schedule 1: Lucy and John Matterocci

*Income earned from work: IRS Form 1040--Line 1 , Schedule 1--Lines 12 and 18 , Schedule K-1 (IRS Form 10

65)--Box 14 (Code A). If any individual earning item is

negative, do not include that item in your calculation.

6

© 2019

NASFAA. All rights reserved.

Sample IRS Form 1040 Schedule 2 (not filed by Lucy and John)

7

© 2019

NASFAA. All rights reserved.

Sample IRS Form 1040 Schedule 3 (not filed by Lucy and John)

8

© 2019 NASFAA. All rights reserved.

Sample Tax Transcript 1040: Lucy and John Matterocci

1040: p.1

1040: 1

1040: 2a

Sch 1: 12

1040: 4a

1040: 4b

1040: p.1

*

**

*Income earned from work: IRS Form 1040–Line 1 , Schedule 1–Lines 12 and 18 , Schedule K-1 (IRS Form 1065)–Box 14 (Code A). If any individual earning item

is negative, do not include that item in your calculation.

**Value of '0' denotes schedule was not filed.

© 2019 NASFAA. All rights reserved.

Internal Revenue Service

United States Department of the Treasury

This Product Contains Sensitive Taxpayer Data

Request Date: 08-30-2019

Response Date: 08-30-2019

Tracking Number: XXXXXXXXXXXX

Tax Return Transcript

SSN Provided: XXX-XX-1614

Tax Period Ending: Dec. 31, 2018

The following items reflect the amount as shown on the return (PR), and the amount as

adjusted (PC), if applicable. They do not show subsequent activity on the account.

SSN: XXX-XX-1614

SPOUSE SSN: XXX-XX-7145

NAME(S) SHOWN ON RETURN: LUCY JOHN MATT

FILING STATUS:

FORM NUMBER:

CYCLE POSTED:

RECEIVED DATE:

REMITTANCE:

EXEMPTION NUMBER:

OTHER DEPENDENT CREDIT TOTAL ELIGIBLE PER COMPUTER:

OTHER DEPENDENT CREDIT TOTAL ELIGIBLE VERIFIED:

EXEMPTION NUMBER:

DEPENDENT 1 NAME CTRL:

Married Filed Joint

1040

20191205

Apr.15, 2019

$0.00

05

01

00

05

DELU

DEPENDENT 1 SSN: XXX-XX-5630

DEPENDENT 2 NAME CTRL: MATT

DEPENDENT 2 SSN: XXX-XX-7982

DEPENDENT 3 NAME CTRL: MATT

DEPENDENT 3 SSN: XXX-XX-5309

DEPENDENT 4 NAME CTRL:

DEPENDENT 4 SSN:

PTIN:

PREPARER EIN:

Income

WAGES, SALARIES, TIPS, ETC:......................................................$122,179.00

TAXABLE INTEREST INCOME: SCH B:....................................................$2,208.00

TAX-EXEMPT INTEREST:...................................................................$0.00

ORDINARY DIVIDEND INCOME: SCH B:.......................................................$0.00

QUALIFIED DIVIDENDS:...................................................................$0.00

REFUNDS OF STATE/LOCAL TAXES:........................................................$814.00

ALIMONY RECEIVED:......................................................................$0.00

BUSINESS INCOME OR LOSS (Schedule C):..................................................$0.00

BUSINESS INCOME OR LOSS: SCH C PER COMPUTER:...........................................$0.00

CAPITAL GAIN OR LOSS: (Schedule D):....................................................$0.00

CAPITAL GAINS OR LOSS: SCH D PER COMPUTER:.............................................$0.00

OTHER GAINS OR LOSSES (Form 4797):.....................................................$0.00

TOTAL IRA DISTRIBUTIONS:...............................................................$0.00

TAXABLE IRA DISTRIBUTIONS:.............................................................$0.00

IRAs, PENSIONS AND ANNUITIES:..........................................................$0.00

TAXABLE IRAs, PENSIONS AND ANNUITIES:..................................................$0.00

SCHEDULE 2 INDICATOR:......................................................................0

SCHEDULE 3 INDICATOR:......................................................................0

9

10

Sch 1: 18

Sch 1: 25

Sch 1: 28

Sch 1: 32

1040: 7

*

*Income earned from work: IRS Form 1040–Line 1, Schedule 1–Lines 12 and 18, Schedule K-1 (IRS Form 1065)

–Box 14 (Code A) . If any individual earning

item is negative, do not include that item in your calculation.

© 2019 NASFAA. All rights reserved.

ADDITIONAL INCOME:.................................................................$8,110.00

ADDITIONAL INCOME PER COMPUTER:....................................................$8,110.00

REFUNDABLE CREDITS PER COMPUTER:.......................................................$0.00

REFUNDABLE EDUCATION CREDIT PER COMPUTER:..............................................$0.00

QUALIFIED BUSINESS INCOME DEDUCTION:...................................................$0.00

RENT/ROYALTY/PARTNERSHIP/ESTATE (Schedule E):..........................................$0.00

RENT/ROYALTY/PARTNERSHIP/ESTATE (Schedule E) PER COMPUTER:.............................$0.00

RENT/ROYALTY INCOME/LOSS PER COMPUTER:.................................................$0.00

ESTATE/TRUST INCOME/LOSS PER COMPUTER:.................................................$0.00

PARTNERSHIP/S-CORP INCOME/LOSS PER COMPUTER PER COMPUTER:..............................$0.00

FARM INCOME OR LOSS (Schedule F):......................................................$0.00

FARM INCOME OR LOSS (Schedule F) PER COMPUTER:.........................................$0.00

UNEMPLOYMENT COMPENSATION:.........................................................$7,296.00

TOTAL SOCIAL SECURITY BENEFITS:........................................................$0.00

TAXABLE SOCIAL SECURITY BENEFITS:......................................................$0.00

TAXABLE SOCIAL SECURITY BENEFITS PER COMPUTER:.........................................$0.00

OTHER INCOME:..........................................................................$0.00

SCHEDULE EIC SE INCOME PER COMPUTER:...................................................$0.00

SCHEDULE EIC EARNED INCOME PER COMPUTER:...............................................$0.00

SCH EIC DISQUALIFIED INC COMPUTER:.....................................................$0.00

TOTAL INCOME:....................................................................$132,497.00

TOTAL INCOME PER COMPUTER:.......................................................$132,497.00

Adjustments to Income

EDUCATOR EXPENSES:.....................................................................$0.00

EDUCATOR EXPENSES PER COMPUTER:........................................................$0.00

RESERVIST AND OTHER BUSINESS EXPENSE:..................................................$0.00

HEALTH SAVINGS ACCT DEDUCTION:.........................................................$0.00

HEALTH SAVINGS ACCT DEDUCTION PER COMPTR:..............................................$0.00

MOVING EXPENSES: F3903:................................................................$0.00

SELF EMPLOYMENT TAX DEDUCTION:.........................................................$0.00

SELF EMPLOYMENT TAX DEDUCTION PER COMPUTER:............................................$0.00

SELF EMPLOYMENT TAX DEDUCTION VERIFIED:................................................$0.00

KEOGH/SEP CONTRIBUTION DEDUCTION:......................................................$0.00

SELF-EMP HEALTH INS DEDUCTION:.........................................................$0.00

EARLY WITHDRAWAL OF SAVINGS PENALTY:...................................................$0.00

ALIMONY PAID SSN:...........................................................................

ALIMONY PAID:..........................................................................$0.00

IRA DEDUCTION:.........................................................................$0.00

IRA DEDUCTION PER COMPUTER:............................................................$0.00

STUDENT LOAN INTEREST DEDUCTION:.......................................................$0.00

STUDENT LOAN INTEREST DEDUCTION PER COMPUTER:..........................................$0.00

STUDENT LOAN INTEREST DEDUCTION VERIFIED:..............................................$0.00

TUITION AND FEES DEDUCTION:............................................................$0.00

TUITION AND FEES DEDUCTION PER COMPUTER:...............................................$0.00

DOMESTIC PRODUCTION ACTIVITIES DEDUCTION:..............................................$0.00

DOMESTIC PRODUCTION ACTIVITIES DEDUCTION PER COMPUTER:.................................$0.00

OTHER ADJUSTMENTS:.....................................................................$0.00

ARCHER MSA DEDUCTION:..................................................................$0.00

ARCHER MSA DEDUCTION PER COMPUTER:.....................................................$0.00

TOTAL ADJUSTMENTS:.....................................................................$0.00

TOTAL ADJUSTMENTS PER COMPUTER:........................................................$0.00

ADJUSTED GROSS INCOME:...........................................................$132,497.00

ADJUSTED GROSS INCOME PER COMPUTER:..............................................$132,497.00

Tax and Credits

65-OR-OVER:...............................................................................NO

BLIND:....................................................................................NO

SPOUSE 65-OR-OVER:........................................................................NO

SPOUSE BLIND:.............................................................................NO

STANDARD DEDUCTION PER COMPUTER:..................................................$24,000.00

ADDITIONAL STANDARD DEDUCTION PER COMPUTER:............................................$0.00

TAX TABLE INCOME PER COMPUTER:...................................................$108,497.00

EXEMPTION AMOUNT PER COMPUTER:.........................................................$0.00

TAXABLE INCOME:..................................................................$108,497.00

TAXABLE INCOME PER COMPUTER:.....................................................$108,497.00

11

Sch 3: 50

Sch 2: 46

1040: 13

Sch 2: 46

*

**

***If Income Tax Paid is negative, use zero.

© 2019 NASFAA. All rights reserved.

TOTAL POSITIVE INCOME PER COMPUTER:..............................................$132,497.00

TENTATIVE TAX:....................................................................$15,748.00

TENTATIVE TAX PER COMPUTER:.......................................................$15.748.00

FORM 8814 ADDITIONAL TAX AMOUNT:.......................................................$0.00

TAX ON INCOME LESS SOC SEC INCOME PER COMPUTER:........................................$0.00

FORM 6251 ALTERNATIVE MINIMUM TAX:.....................................................$0.00

FORM 6251 ALTERNATIVE MINIMUM TAX PER COMPUTER:........................................$0.00

FOREIGN TAX CREDIT:....................................................................$0.00

FOREIGN TAX CREDIT PER COMPUTER:.......................................................$0.00

FOREIGN INCOME EXCLUSION PER COMPUTER:.................................................$0.00

FOREIGN INCOME EXCLUSION TAX PER COMPUTER:.............................................$0.00

EXCESS ADVANCE PREMIUM TAX CREDIT REPAYMENT AMOUNT:....................................$0.00

EXCESS ADVANCE PREMIUM TAX CREDIT REPAYMENT VERIFIED AMOUNT:...........................$0.00

CHILD & DEPENDENT CARE CREDIT:.........................................................$0.00

CHILD & DEPENDENT CARE CREDIT PER COMPUTER:............................................$0.00

CREDIT FOR ELDERLY AND DISABLED:.......................................................$0.00

CREDIT FOR ELDERLY AND DISABLED PER COMPUTER:..........................................$0.00

EDUCATION CREDIT:......................................................................$0.00

EDUCATION CREDIT PER COMPUTER:.........................................................$0.00

GROSS EDUCATION CREDIT PER COMPUTER:...................................................$0.00

RETIREMENT SAVINGS CNTRB CREDIT:.......................................................$0.00

RETIREMENT SAVINGS CNTRB CREDIT PER COMPUTER:..........................................$0.00

PRIM RET SAV CNTRB: F8880 LN6A:........................................................$0.00

SEC RET SAV CNTRB: F8880 LN6B:.........................................................$0.00

TOTAL RETIREMENT SAVINGS CONTRIBUTION: F8880 CMPTR:....................................$0.00

RESIDENTIAL ENERGY CREDIT:.............................................................$0.00

RESIDENTIAL ENERGY CREDIT PER COMPUTER:................................................$0.00

CHILD AND OTHER DEPENDENT CREDIT:..................................................$4,500.00

CHILD AND OTHER DEPENDENT CREDIT PER COMPUTER:.....................................$4,500.00

ADOPTION CREDIT: F8839:................................................................$0.00

ADOPTION CREDIT PER COMPUTER:..........................................................$0.00

FORM 8396 MORTGAGE CERTIFICATE CREDIT:.................................................$0.00

FORM 8396 MORTGAGE CERTIFICATE CREDIT PER COMPUTER:....................................$0.00

F3800, F8801 AND OTHER CREDIT AMOUNT:..................................................$0.00

FORM 3800 GENERAL BUSINESS CREDITS:....................................................$0.00

FORM 3800 GENERAL BUSINESS CREDITS PER COMPUTER:.......................................$0.00

PRIOR YR MIN TAX CREDIT: F8801:........................................................$0.00

PRIOR YR MIN TAX CREDIT: F8801 PER COMPUTER:...........................................$0.00

F8936 ELECTRIC MOTOR VEHICLE CREDIT AMOUNT:............................................$0.00

F8936 ELECTRIC MOTOR VEHICLE CREDIT PER COMPUTER:......................................$0.00

F8910 ALTERNATIVE MOTOR VEHICLE CREDIT AMOUNT:.........................................$0.00

F8910 ALTERNATIVE MOTOR VEHICLE CREDIT PER COMPUTER:...................................$0.00

OTHER CREDITS:.........................................................................$0.00

TOTAL CREDITS:.....................................................................$4,500.00

TOTAL CREDITS PER COMPUTER:........................................................$4,500.00

INCOME TAX AFTER CREDITS PER COMPUTER:............................................$11,248.00

*** “Income Tax After Credits Per Computer”

$11,248.00

‒ ** “Excess Advance Premimum Tax Credit Repayment Amount”

‒

$0.00

= **** Income Tax Paid

= $11,248.00

Other Taxes

SE TAX:................................................................................$0.00

SE TAX PER COMPUTER:...................................................................$0.00

SOCIAL SECURITY AND MEDICARE TAX ON UNREPORTED TIPS:...................................$0.00

SOCIAL SECURITY AND MEDICARE TAX ON UNREPORTED TIPS PER COMPUTER:......................$0.00

TAX ON QUALIFIED PLANS F5329 (PR):.....................................................$0.00

TAX ON QUALIFIED PLANS F5329 PER COMPUTER:.............................................$0.00

IRAF TAX PER COMPUTER:.................................................................$0.00

TP TAX FIGURES (REDUCED BY IRAF) PER COMPUTER:....................................$11,248.00

IMF TOTAL TAX (REDUCED BY IRAF) PER COMPUTER:.....................................$11,248.00

TOTAL OTHER TAXES PER COMPUTER:........................................................$0.00

UNPAID FICA ON REPORTED TIPS:..........................................................$0.00

F8959-8960 OTHER TAXES:................................................................$0.00

‒

12

© 2019 NASFAA. All rights reserved.

TOTAL OTHER TAXES:.....................................................................$0.00

RECAPTURE TAX: F8611:..................................................................$0.00

HOUSEHOLD EMPLOYMENT TAXES:............................................................$0.00

HOUSEHOLD EMPLOYMENT TAXES PER COMPUTER:...............................................$0.00

HEALTH CARE RESPONSIBILITY PENALTY:....................................................$0.00

HEALTH CARE RESPONSIBILITY PENALTY VERIFIED:...........................................$0.00

HEALTH COVERAGE RECAPTURE: F8885:......................................................$0.00

RECAPTURE TAXES:.......................................................................$0.00

TOTAL ASSESSMENT PER COMPUTER:....................................................$11,248.00

TOTAL TAX LIABILITY TP FIGURES:...................................................$11,248.00

TOTAL TAX LIABILITY TP FIGURES PER COMPUTER:......................................$11,248.00

Payments

FEDERAL INCOME TAX WITHHELD:......................................................$11,272.00

HEALTH CARE: INDIVIDUAL RESPONSIBILTY:.................................................$0.00

HEALTH CARE FULL-YEAR COVERAGE INDICATOR:..................................................1

ESTIMATED TAX PAYMENTS:................................................................$0.00

OTHER PAYMENT CREDIT:..................................................................$0.00

REFUNDABLE EDUCATION CREDIT:...........................................................$0.00

REFUNDABLE EDUCATION CREDIT PER COMPUTER:..............................................$0.00

REFUNDABLE EDUCATION CREDIT VERIFIED:..................................................$0.00

REFUNDABLE CREDITS:....................................................................$0.00

EARNED INCOME CREDIT:..................................................................$0.00

EARNED INCOME CREDIT PER COMPUTER:.....................................................$0.00

EARNED INCOME CREDIT NONTAXABLE COMBAT PAY:............................................$0.00

SCHEDULE 8812 NONTAXABLE COMBAT PAY:...................................................$0.00

EXCESS SOCIAL SECURITY & RRTA TAX WITHHELD:............................................$0.00

SCHEDULE 8812 TOT SS/MEDICARE WITHHELD:................................................$0.00

SCHEDULE 8812 ADDITIONAL CHILD TAX CREDIT:.............................................$0.00

SCHEDULE 8812 ADDITIONAL CHILD TAX CREDIT PER COMPUTER:................................$0.00

SCHEDULE 8812 ADDITIONAL CHILD TAX CREDIT VERIFIED:....................................$0.00

AMOUNT PAID WITH FORM 4868:............................................................$0.00

FORM 2439 REGULATED INVESTMENT COMPANY CREDIT:.........................................$0.00

FORM 4136 CREDIT FOR FEDERAL TAX ON FUELS:.............................................$0.00

FORM 4136 CREDIT FOR FEDERAL TAX ON FUELS PER COMPUTER:................................$0.00

HEALTH COVERAGE TX CR: F8885:..........................................................$0.00

SEC 965 TAX INSTALLMENT:...............................................................$0.00

SEC 965 TAX LIABILITY:.................................................................$0.00

PREMIUM TAX CREDIT AMOUNT:.............................................................$0.00

PREMIUM TAX CREDIT VERIFIED AMOUNT:....................................................$0.00

PRIMARY NAP FIRST TIME HOME BUYER INSTALLMENT AMT:.....................................$0.00

SECONDARY NAP FIRST TIME HOME BUYER INSTALLMENT AMT:...................................$0.00

FIRST TIME HOMEBUYER CREDIT REPAYMENT AMOUNT:..........................................$0.00

FORM 5405 TOTAL HOMEBUYERS CREDIT REPAYMENT PER COMPUTER:..............................$0.00

SMALL EMPLOYER HEALTH INSURANCE PER COMPUTER:..........................................$0.00

SMALL EMPLOYER HEALTH INSURANCE PER COMPUTER (2):......................................$0.00

FORM 2439 AND OTHER CREDITS:...........................................................$0.00

TOTAL PAYMENTS:...................................................................$11,272.00

TOTAL PAYMENTS PER COMPUTER:......................................................$11,272.00

Refund or Amount Owed

REFUND AMOUNT:.......................................................................$-24.00

APPLIED TO NEXT YEAR’S ESTIMATED TAX:..................................................$0.00

ESTIMATED TAX PENALTY:.................................................................$0.00

TAX ON INCOME LESS STATE REFUND PER COMPUTER:..........................................$0.00

BAL DUE/OVER PYMT USING TP FIG PER COMPUTER:.........................................$-24.00

BAL DUE/OVER PYMT USING COMPUTER FIGURES:............................................$-24.00

FORM 8888 TOTAL REFUND PER COMPUTER:...................................................$0.00

Third Party Designee

THIRD PARTY DESIGNEE ID NUMBER:.............................................................

AUTHORIZATION INDICATOR:...................................................................0

THIRD PARTY DESIGNEE NAME:..................................................................

113

© 2019 NASFAA. All rights reserved.

Interest and Dividends

GROSS SCHEDULE B INTEREST:.........................................................$2,208.00

TAXABLE INTEREST INCOME:...........................................................$2,208.00

EXCLUDABLE SAVINGS FROM BOND INT:......................................................$0.00

GROSS SCHEDULE B DIVIDENDS:............................................................$0.00

DIVIDEND INCOME:.......................................................................$0.00

FOREIGN ACCOUNTS IND:...................................................................NONE

REQUIRED TO FILE FINCEN FORM 114:.......................................................NONE

Form 8863 – Education Credits (Hope and Lifetime Learning Credits)

PART III – ALLOWABLE EDUCATION CREDITS

GROSS EDUCATION CR PER COMPUTER:.......................................................$0.00

TOTAL EDUCATION CREDIT AMOUNT:.........................................................$0.00

TOTAL EDUCATION CREDIT AMOUNT PER COMPUTER:............................................$0.00

This Product Contains Sensitive Taxpayer Data

This page intentionally left blank.

14

Appendices

Appendix A

Sample 2018 W-2 Form, Reference Guide for Box 12 Codes, and Sample Form W-2 Wage and Tax Statement

Appendix B

Criteria for 2020-21 Simplified Needs Formulas and Automatic Zero EFC Calculation

Appendix C

2018 IRS Form 1040: Indicators That Schedule 1, 2 or 3 was Required

Appendix D

Current Year Transcript Availability

Appendix E

References, Resources and Websites – Tax Returns and Transcripts

15

© 2019

NASFAA. All rights reserved.

Appendix A

Sample 2018 W-2 Form

In addition to wages earned, the W-2 form may reveal sources of untaxed income, such as payments to tax-deferred pension and

savings plan amounts reported in boxes 12a through 12d, code D, E, F, G, H and S.

Schools are not required to review income listed in box 14, however if you are aware that a box 14 item should be reported (i.e. clergy

parsonage allowances) then you would count that amount as untaxed income.

Form W-2 Reference Guide for Box 12 Codes

A

Uncollected social security or RRTA tax on tips

K

20% excise tax on excess golden parachute

payments

V

Income from exercise of nonstatutory stock

option(s)

B

Uncollected Medicare tax on tips

L

Substantiated employee business expense

reimbursements

W

Employer contributions (including amounts

employee elected to contribute using a cafeteria

plan) to employee’s health savings account

C

Taxable cost of group-term life insurance over

$50,000

M

Uncollected social security or RRTA tax on

taxable cost of group-term life insurance over

$50,000 (former employees only)

Y

Deferrals under a section 409A nonqualified

deferred compensation plan

D

Elective deferrals to a section 401(k) cash or

deferred arrangement (including deferrals

under a SIMPLE 401(k) arrangement)

N

Uncollected Medicare tax on taxable cost of

group-term life insurance over $50,000 (former

employees only)

Z

Income under a nonqualified deferred

compensation plan that fails to satisfy section

409A

E

Elective deferrals under a section 403(b)

salary reduction agreement

P

Excludable moving expense reimbursements

paid directly to a member of the U.S. Armed

Forces

AA

Designated Roth contributions under a section

401(k) plan

F

Elective deferrals under a section 408(k)(6)

salary reduction SEP

Q

Nontaxable combat pay

BB

Designated Roth contributions under a section

403(b) plan

G

Elective deferrals and employer contributions

(including nonelective deferrals) to a section

457(b) deferred compensation plan

R

Employer contributions to an Archer MSA

DD

Cost of employer-sponsored health coverage

H

Elective deferrals to a section 501(c)(18)(D)

tax-exempt organization plan

S

Employee salary reduction contributions under

a section 408(p) SIMPLE plan

EE

Designated Roth contributions under a

governmental section 457(b) plan

J

Nontaxable sick pay

T

Adoption benefits

FF

Permitted benefits under a qualified small

employer health reimbursement arrangement

(For additional codes and complete descriptions, visit https://www.irs.gov/pub/irs-pdf/fw2_18.pdf)

16

© 2019 NASFAA. All rights reserved.

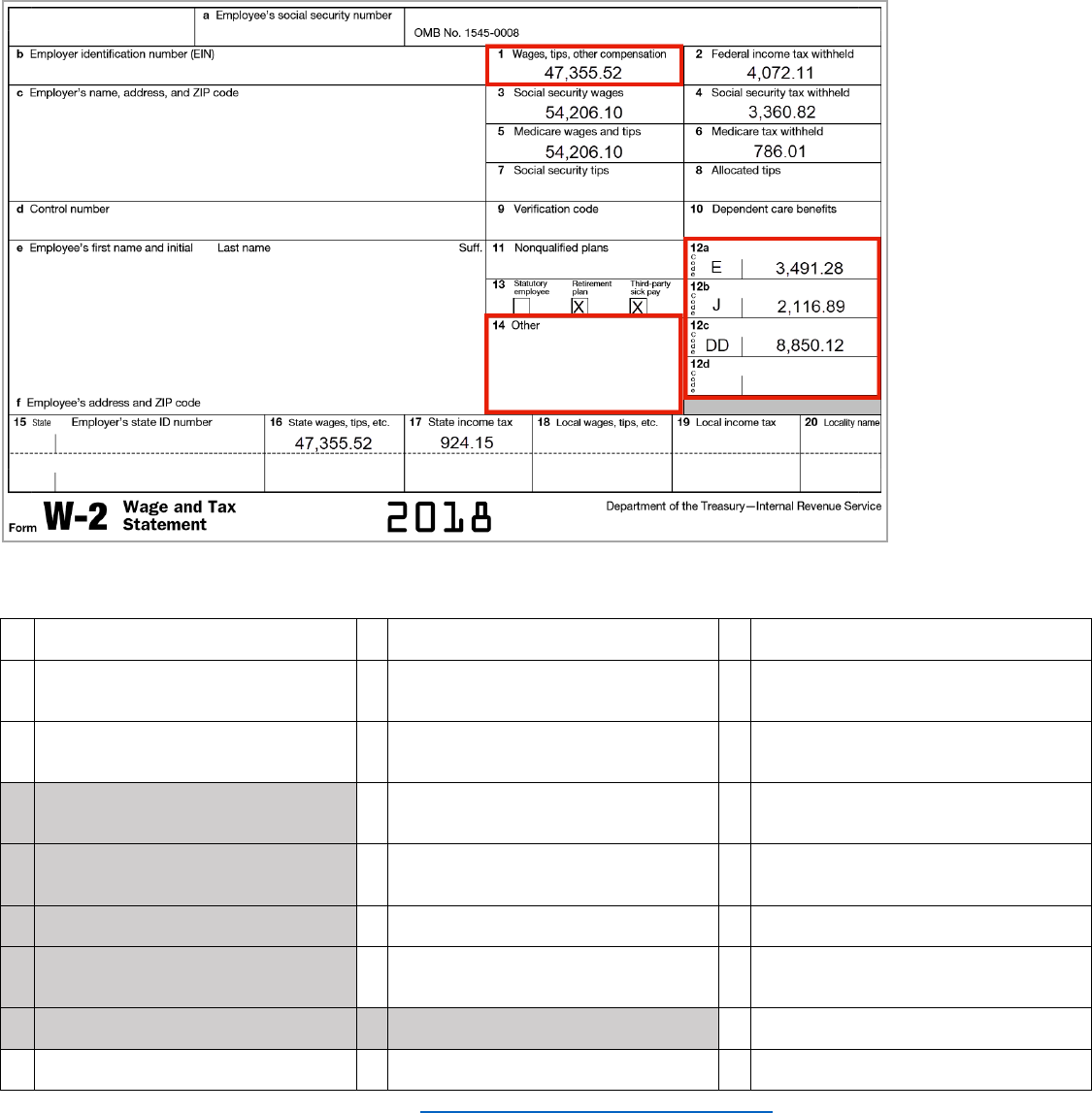

Sample 2018 W-2 Wage and Tax Statement

Internal Revenue Service

United States Department of the Treasury

This Product Contains Sensitive Taxpayer Data

Request Date: 08-30-2019

Response Date: 08-30-2019

Tracking Number: XXXXXXXXXXXX

*

Wage and Income Transcript

SSN Provided: XXX-XX-1614

Tax Period Ending: December 2018

Form W-2 Wage and Tax Statement

Employer:

Employer Identification Number (EIN):

Employee:

Employee’s Social Security Number: XXX-XX-1614

LUCY JANI MATT

1234 W

Submission Type:................................................Original document

Wages, Tips and Other Compensation:....................................$47,355.00 - - - - - Box 1

Federal Income Tax Withheld:............................................$4,072.00

-

- Box 2

Social Security Wages:.................................................$54,206.00

- - - - - Box 3

Social Security Tax Withheld:...........................................$3,360.00

-

- Box 4

Medicare Wages and Tips:...............................................$54,206.00

- - - - - Box 5

Medicare Tax Withheld:....................................................$786.00

- - Box 6

Social Security Tips:.......................................................$0.00

- - - - - Box 7

Allocated Tips:.............................................................$0.00

- - Box 8

Dependent Care Benefits:....................................................$0.00

- - - - - Box 10

Deferred Compenensation:................................................$3,491.00

- - Box 12a-d (D, E, F, G, H)

Code “Q” Nontaxable Combat Pay:.............................................$0.00

Code “W” Employer Contributions to a Health Savings Account:................$0.00

Code “Y” Deferrals under a section 409A nonqualified Deferred Compensation

plan:.......................................................................$0.00

Code “Z” Income under section 409A on a nonqualified Deferred Compensation

plan:.......................................................................$0.00

Code “R” Employer’s Contribution to MSA:....................................$0.00

Code “S” Employer’s Contribution to Simple Account:.........................$0.00

- - - - - Box 12a-d (S)

Code “T” Expenses Incurred for Qualified Adoptions:.........................$0.00

Code “V” Income from exercise of non-statutory stock options:...............$0.00

Code “AA” Designated Roth Contributions under a Section 401(k) Plan:........$0.00

Code “BB” Designated Roth Contributions under a Section 403(b) Plan:........$0.00

Code “DD” Cost of Employer-Sponsored Health Coverage:...................$8,850.00

Code “EE” Designated ROTH Contributions Under a Governmental Section 457(b)

Plan:.......................................................................$0.00

Code “FF” Permitted benefits under a qualified small employer health

reimbursement arrangement:..................................................$0.00

* Current tax year information may not be available until July.

Note: Payments to tax-deferred pension and retirement savings plans under “Deferred Compensation” and “Code ‘S’ Employer’s Contribution to Simple

Account” are not required to be verified unless there is conflicting information. “Deferred Compensation” is assumed to include W-2 Box 12a to 12d,

Codes D, E, F, G, and H. If the total for this line plus the line for Code ‘S’ do not match the amount reported on the FAFSA, the school will need to collect

additional documentation from the student or parent, as applicable. Schools may obtain a signed statement indicating the correct amounts or some

other documentation the school deems appropriate to resolve the conflict.

17

© 2019 NASFAA. All rights reserved.

This page intentionally left blank.

18

Appendix B

Criteria for 2020-21 Simplified Needs Formulas and Automatic Zero EFC Calculation

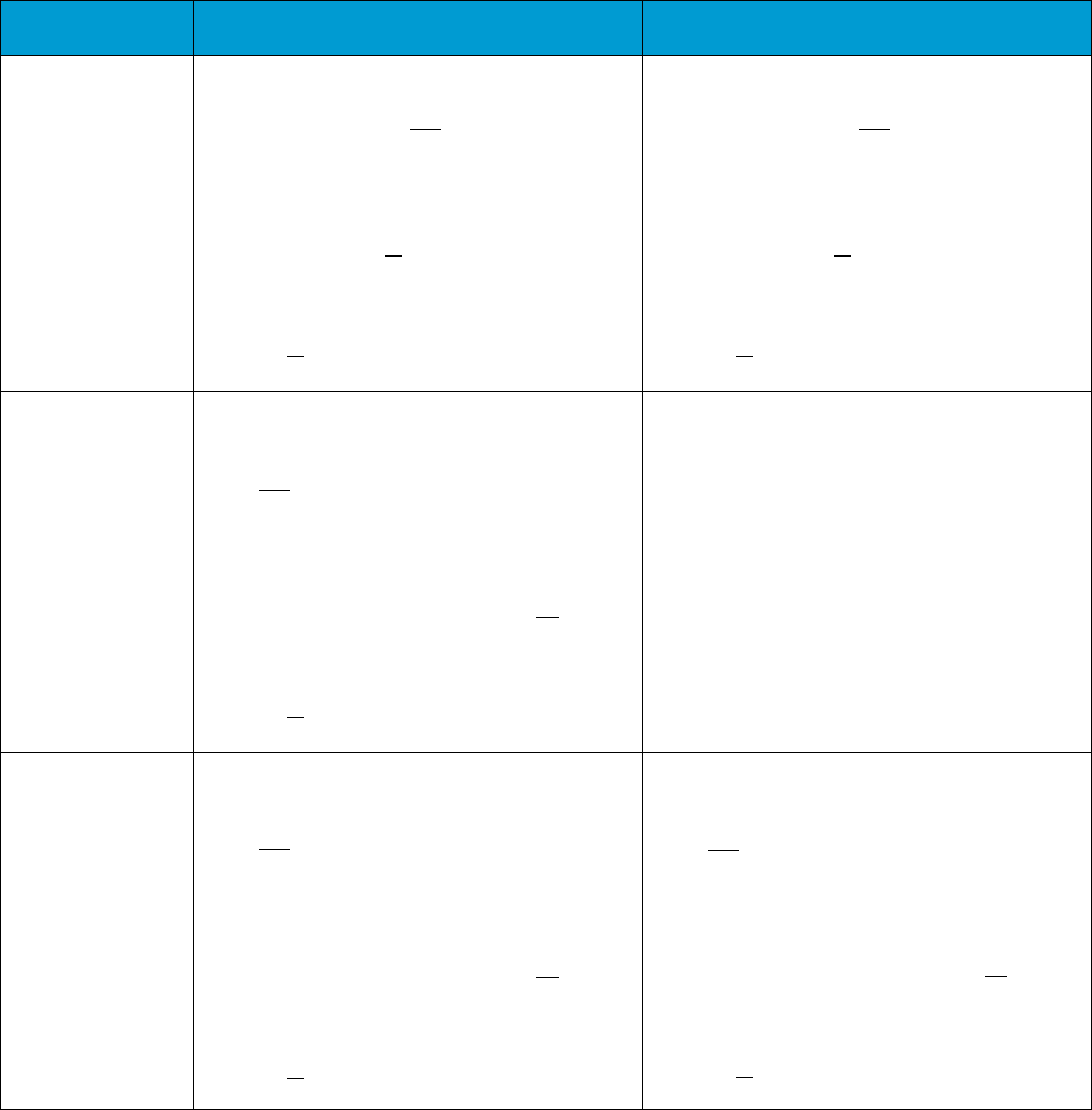

The following criteria is used to determine if students qualify to have their EFCs calculated using a simplified formula.

Simplified

(assets not considered)

Automatic Zero EFC

Formula A

Dependent student

Parents had a 2018 AGI of $49,999 or less (for tax

filers), or if non-filers, income earned from work in

2018 is $49,999 or less; and

Either

- Parents filed a 2018 IRS Form 1040, but did not

file a Schedule 1*, filed a tax form from a Trust

Territory**, or were not required to file any

income tax return or

- Anyone in the parents’ household size (as

defined on the FAFSA) received any designated

means-tested federal benefits*** during 2018 or

2019, or

- Parent is a dislocated worker.

Parents had a 2018 AGI of $26,000 or less (for tax

filers), or if non-filers, income earned from work in

2018 is $26,000 or less; and

Either

- Parents filed a 2018 IRS Form 1040, but did not

file a Schedule 1*, filed a tax form from a Trust

Territory**, or were not required to file any

income tax return or

- Anyone in the parents’ household size (as

defined on the FAFSA) received any designated

means-tested federal benefits*** during 2018 or

2019, or

- Parent is a dislocated worker.

Formula B

Independent student

without dependents

(other than a spouse)

Student (and spouse, if any) had a 2018 AGI of

$49,999 or less (for tax filers), or if non-filers,

income earned from work in 2018 is $49,999 or

less; and

Either

- Student (and spouse, if any) filed a 2018 IRS

Form 1040, but did not file a Schedule 1*, filed a

tax form from a Trust Territory**, or were not

required to file any income tax return or

- Anyone in the student’s household size (as

defined on the FAFSA) received any designated

means-tested federal benefits*** during 2018 or

2019, or

- Student (or spouse, if any) is a dislocated worker.

Not applicable.

Formula C

Independent student

with dependents

(other than a spouse)

Student (and spouse, if any) had a 2018 AGI of

$49,999 or less (for tax filers), or if non-filers,

income earned from work in 2018 is $49,999 or

less; and

Either

- Student (and spouse, if any) filed a 2018 IRS

Form 1040, but did not file a Schedule 1*, filed a

tax form from a Trust Territory**, or were not

required to file any income tax return or

- Anyone in the student’s household size (as

defined on the FAFSA) received any designated

means-tested federal benefits*** during 2018 or

2019, or

- Student (or spouse, if any) is a dislocated worker.

Student (and spouse, if any) had a 2018 AGI of

$26,000 or less (for tax filers), or if non-filers,

income earned from work in 2018 is $26,000 or

less; and

Either

- Student (and spouse, if any) filed a 2018 IRS

Form 1040, but did not file a Schedule 1*, filed a

tax form from a Trust Territory**, or were not

required to file any income tax return or

- Anyone in the student’s household size (as

defined on the FAFSA) received any designated

means-tested federal benefits*** during 2018 or

2019, or

- Student (or spouse, if any) is a dislocated worker.

*May also qualify if Schedule 1 was filed to report only a capital gain (line 13 – may not be a negative value), unemployment compensation (line 19),

other income to report an Alaska Permanent Fund dividend (line 21 – may not a negative value), educator expenses (line 23), IRA deduction (line 32),

and/or student loan interest deduction (line 33).

**Trust Territory: Commonwealth of Puerto Rico, Guam, American Samoa, the U.S. Virgin Islands, the Republic of the Marshall Islands, the Federated

States of Micronesia, or Palau.

***Benefits include Medicaid, Supplemental Security Income (SSI), Supplemental Nutrition Assistance (SNAP), Free or Reduced Price School Lunch,

Temporary Assistance for Needy Families (TANF), and Special Supplemental Nutrition Program for Women, Infants and Children (WIC).

19

© 2019

NASFAA. All rights reserved.

Appendix C

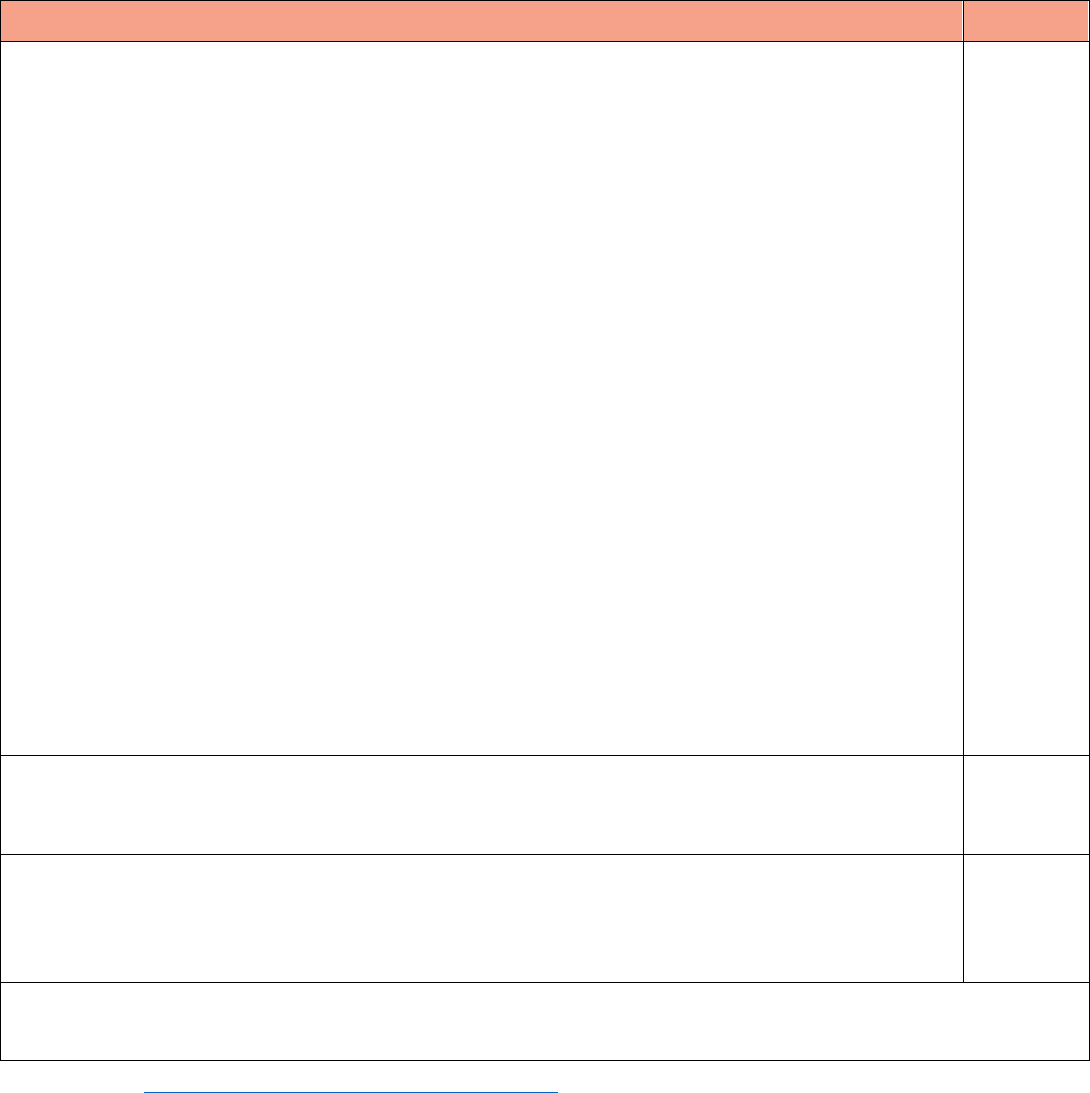

2018 IRS Form 1040 – Indicators That Schedule 1, 2 or 3 was Required

Many taxpayers will only need to file Form 1040 and no schedules. Those with more complicated tax returns

will need to complete one or more of the 2018 Form 1040 Schedules along with their Form 1040. These

taxpayers include people claiming certain deductions or credits or owing additional taxes. Below is a general

guide indicating whether Schedules 1, 2, or 3 need to be filed based on specific circumstances. Under these

conditions, the school should receive a copy of that schedule to complete verification.

IF YOU… THEN USE…

Have additional income, such as capital gains, unemployment compensation, prize or award money, or

gambling winnings.

Have any deductions to claim, such as student loan interest deduction, self-employment tax, or educator

expenses.

1040 Line 6: Schedule 1 is completed if there is an amount on the inner line of 1040 Line 6

(representing an amount from Schedule 1, Line 22).

1040 Line 7: Schedule 1 is completed if the amount on 1040 Line 7 is not equal to the amount on

Line 6 (representing an amount from Schedule 1, Line 36).

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

NEW: 2020-21 FAFSA questions #35 (S) and #82 (P) ask if Schedule 1 was (or will be) filed with a 2018 tax

return. A note on p. 9 of the FAFSA reads:

Answer “No” if you (and if married, your spouse) did not file a Schedule 1.

Answer “No” if you (and if married, your spouse) did or will file a Schedule 1 to report only one or more of

the following items:

1. Capital gain (line 13 – may not be a negative value)

2. Unemployment compensation (line 19)

3. Other income to report an Alaska Permanent Fund dividend (line 21 – may not be a negative value)

4. Educator expenses (line 23)

5. IRA deduction (line 32)

6. Student loan interest deduction (line 33)

Answer “Yes” if you (or if married, your spouse) filed or will file a Schedule 1 and reported additional

income or adjustments to income on any lines other than or in addition to the six exceptions listed above.

Schedule 1

Owe alternative minimum tax or need to make an excess advance premium tax credit repayment.

1040 Line 11: Schedule 2 is completed if the box for 1040 Line 11b is checked.

Schedule 2

Can claim a nonrefundable credit other than the child tax credit or the credit for other dependents, such

as the foreign tax credit, education credits, or general business credit.

1040 Line 12: Schedule 3 is completed if the box for 1040 Line 12b is checked.

Schedule 3

Note: Besides Schedules 1, 2, and 3, the school does not need to collect copies of IRS schedules of forms that are attached to the

tax return, unless there is conflicting information in the student’s file that needs to be resolved.

Adapted from: https://www.irs.gov/pub/irs-pdf/i1040gi.pdf

20

© 2019

NASFAA. All rights reserved.

Sample 2018 IRS Form 1040 – Page 2

21

© 2019

NASFAA. All rights reserved.

Appendix D

Current Year Transcript Availability

Use the table below to determine the general timeframe when you can request a transcript for a current

year Form 1040 return filed on or before the April due date. Availability varies based on the method you

used to file your return and whether you have a refund or balance due.

Note: If you made estimated tax payments and/or applied your overpayment from a prior year tax return

to your current year tax return, you can request a tax account transcript to confirm these payments or

credits a few weeks after the beginning of the calendar year prior to filing your current year return.

When your original return

shows a …

and you filed electronically,

then

and you filed on paper, then

refund amount or no balance

due,

allow 2-3 weeks after return

submission before you request

a transcript.

allow 6-8 weeks after you

mailed your return before you

request a transcript.

balance due and you paid in full

with your return,

allow 2-3 weeks after return

submission before you request

a transcript.

we process your return in June

and you can request a transcript

in mid to late June.

Note: we process all payments

upon receipt.

balance due and you paid in full

after submitting the return,

allow 3-4 weeks after full

payment before you request a

transcript.

balance due and you didn’t pay

in full,

we process your return in mid-

May and you can request a

transcript by late May.

https://www.irs.gov/individuals/transcript-availability

22

© 2019

NASFAA. All rights reserved.

Appendix E

References, Resources and Websites – Tax Returns and Transcripts

U.S. Department of Education

Federal Registers

Subject: FAFSA Information to be Verified for the 2020-21 Award Year

https://ifap.ed.gov/fregisters/FR052419.html

Electronic Announcements

Subject: 2020-21 Verification Suggested Text Package

https://ifap.ed.gov/eannouncements/073119VerificationSuggestedTextPackage20202021.html

Subject: IRS Announces End to Faxing and Third-Party Mailings of Tax Transcripts

https://ifap.ed.gov/eannouncements/061219IRSAnnEndFaxThirdPartyMailTaxTranscripts.html

Student Aid Eligibility Worksheets

Subject: 2020-21 Free Application for Federal Student Aid (FAFSA®), FAFSA on the Web Worksheet, and the

Student Aid Eligibility Worksheet for Question 23

https://ifap.ed.gov/drugworksheets/2021StudentAidEligibilityWorksheetQ23.html

2019-20 Federal Student Aid Handbook

Application and Verification Guide

- Chapter 2: Filling Out the FAFSA

- Chapter 4: Verification, Updates, and Corrections

https://ifap.ed.gov/fsahandbook/1920FSAHbkAVG.html

Program Integrity Questions and Answers - Verification

https://www2.ed.gov/policy/highered/reg/hearulemaking/2009/verification.html

Federal Student Aid Glossary and Acronyms

https://ifap.ed.gov/fsahandbook/attachments/1819FSAHbkAppendixA.pdf

Internal Revenue Service

Current Year Transcript Availability

https://www.irs.gov/individuals/transcript-availability

Secure Access: How to Register for Certain Online Self-Help Tools

https://www.irs.gov/individuals/secure-access-how-to-register-for-certain-online-self-help-tools

Transcript Types and Ways to Order Them

https://www.irs.gov/individuals/tax-return-transcript-types-and-ways-to-order-them

Get Transcript FAQs

https://www.irs.gov/individuals/get-transcript-faqs

4506T-EZ: Short Form Request for Individual Tax Return Transcript

https://www.irs.gov/pub/irs-pdf/f4506tez.pdf

4506-T: Request for Transcript of Tax Return (transcript and other return information)

https://www.irs.gov/pub/irs-pdf/f4506t.pdf

Here Are Five Facts About the New Form 1040

https://www.irs.gov/newsroom/here-are-five-facts-about-the-new-form-1040

2018 IRS Publication 17, p. 3: Form 1040 Redesign – Helpful Hints

https://www.irs.gov/pub/irs-pdf/i1040gi.pdf

23

© 2019

NASFAA. All rights reserved.