Most Serious Problem #3: Online Records Access

Taxpayer Advocate Service44

Most Serious Problems

MOST SERIOUS PROBLEM #3: ONLINE RECORDS ACCESS

Limited Electronic Access to Taxpayer Records Through

an Online Account Makes Problem Resolution Difficult for

Taxpayers and Results in Inefficient Tax Administration

RESPONSIBLE OFFICIALS

Karen Howard, Director, Office of Online Services

Eric Hylton, Commissioner, Small Business/Self-Employed Division

Kenneth Corbin, Commissioner, Wage and Investment Division

TAXPAYER RIGHTS IMPACTED

1

• e Right to Be Informed

• e Right to Quality Service

• e Right to Pay No More an the Correct Amount of Tax

• e Right to Challenge the IRS’s Position and Be Heard

• e Right to Retain Representation

• e Right to a Fair and Just Tax System

EXPLANATION OF THE PROBLEM

As the IRS moves forward with putting taxpayers first in delivering its strategies, it must continually

emphasize innovation and creativity to ensure success. To provide top quality service, as measured through

the eyes of the taxpayers, the IRS needs to consistently leverage existing technology and identify emerging

programs to pursue innovative solutions and improvements. One area for improvement is its online access

to taxpayer records. Due to limited technology systems, the IRS operates under a largely paper-based system,

requiring taxpayers to keep copies of paper correspondence, call the IRS for assistance, or use a patchwork

of electronic applications to gather necessary information to meet their tax obligations. is system leads to

inefficiencies because taxpayers lack the ability to access necessary filing information, resulting in taxpayer

delays and dissatisfaction with tax administration. Taxpayers must have a simple way to access their IRS tax

records and account information to meet their tax filing and payment obligations.

Despite the many benefits of digital communication and online accounts, it is critical the IRS maintain

telephone and in-person service options. Millions of taxpayers still do not have access to broadband internet,

while other taxpayers strongly prefer to interact with the IRS by telephone or in person for certain categories

1

See

www.TaxpayerAdvocate.irs.gov/taxpayer-rights. The rights contained in the TBOR are also

codified in the IRC.

See

Most Serious Problem #3: Online Records Access

45Annual Report to Congress 2020

Most Serious Problems

of transactions.

2

For these reasons, we believe it is essential that the IRS maintain a robust omnichannel

service environment while it enhances its digital offerings.

3

ANALYSIS

Robust Online Accounts Would Modernize Information Sharing Between the IRS and

Taxpayers

Technology is reshaping how taxpayers and the IRS communicate with each other. e commercial growth

of online services has heightened taxpayers’ expectations for quality online services they can use to conduct

tax communications and transactions. For years, the IRS has steered taxpayers toward digital self-help and

has continuously expanded its offerings of digital service options. However, many of these offerings are

standalone systems, they do not offer complete information, and they are not available to all taxpayers. As the

IRS continues to resume its business operations that were partially or completely shut down at the inception

of the COVID-19 pandemic, it should continue to evaluate what it needs to do to administer the tax laws and

provide necessary taxpayer services, especially under similar conditions in the future.

Because financial institutions and other state tax agencies

4

provide access to key information online, customers

have come to expect secure and convenient access to their personal information with features such as:

• View account balance and tax year or account period details;

• View estimated payments and credits before filing a return;

• View payment history;

• View a list and images of tax returns;

• View a list and images of notices and correspondence;

• View and update contact information;

• View proposed assessments;

• View a list of authorized representatives (tax professional or a tax professional with a power of attorney)

and manage who can access their account;

• View a list of activities that occurred on their account, such as the last time the taxpayer or their

authorized representative accessed the account;

• Calculate a balance due for a date in the future;

• File a power of attorney (POA);

• File a nonresident withholding waiver request;

• Protest a proposed assessment;

• Chat with a customer service representative about confidential matters;

• Send a secure message with attachments;

• Receive an email when a notice or correspondence is sent; and

).

).

See

Most Serious Problem #3: Online Records Access

Taxpayer Advocate Service46

Most Serious Problems

• Allow an authorized representative full or partial access to the taxpayer’s Online Account records and

information.

e National Taxpayer Advocate recognizes the IRS is aware of these customer expectations and is progressing

toward providing similar services as soon as possible. However, due to years of limited funds, the IRS has

only been able to add some online services in a piecemeal fashion. Taxpayers deserve better service from the

IRS. e COVID-19 pandemic highlighted the necessity of robust online services for taxpayers and their

representatives.

Since 2016, the IRS has offered taxpayers an Online Account application. Over time, the capabilities and

popularity of the Online Account have increased. Taxpayers accessed the Online Account application over 23

million times in fiscal year (FY) 2020.

5

As shown in Figure 1.3.1, the IRS has provided several other online

applications to assist taxpayers. Because the Online Account does not reflect all the information from these

other applications, there is no consolidated place where taxpayers can view all their information.

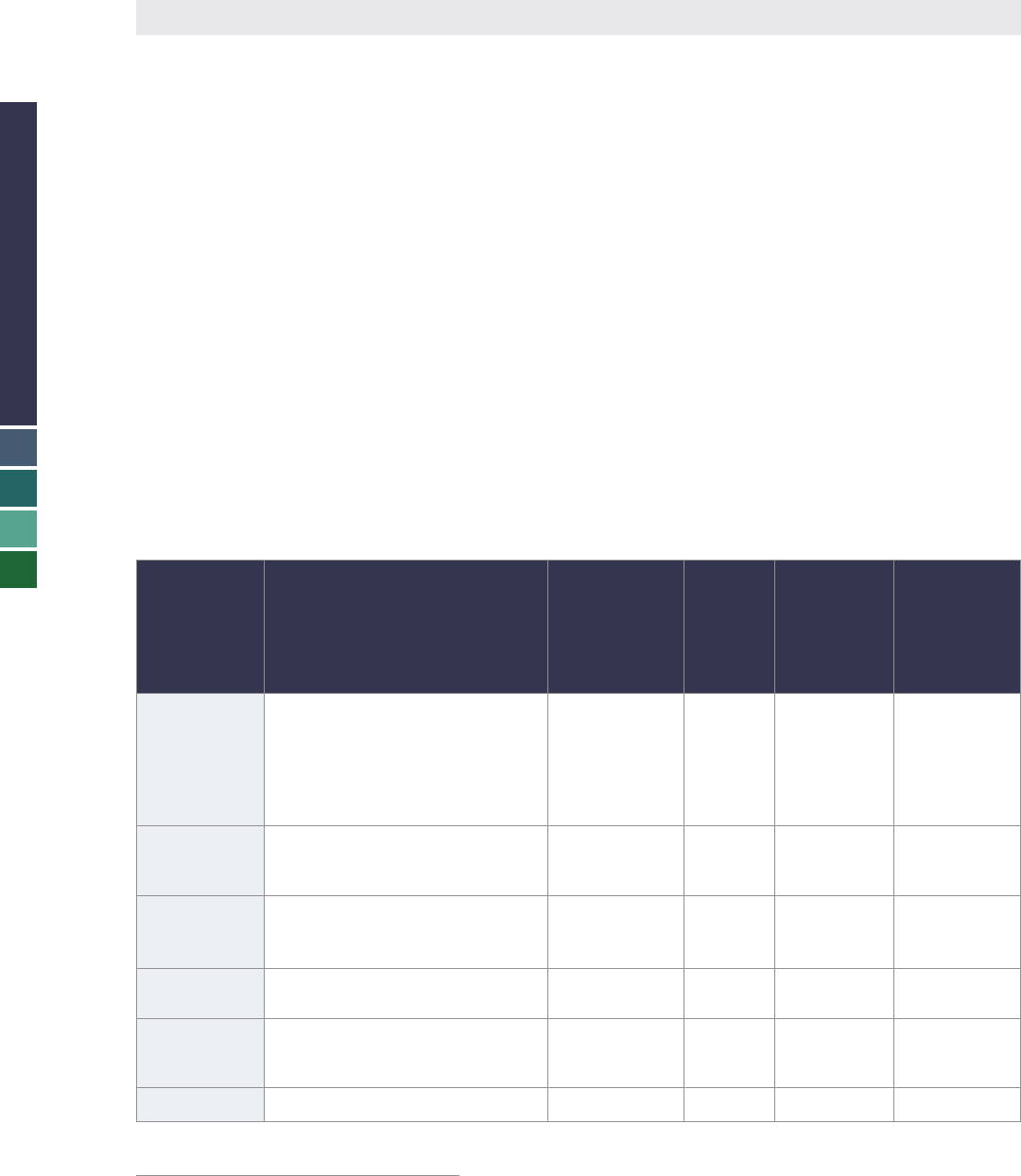

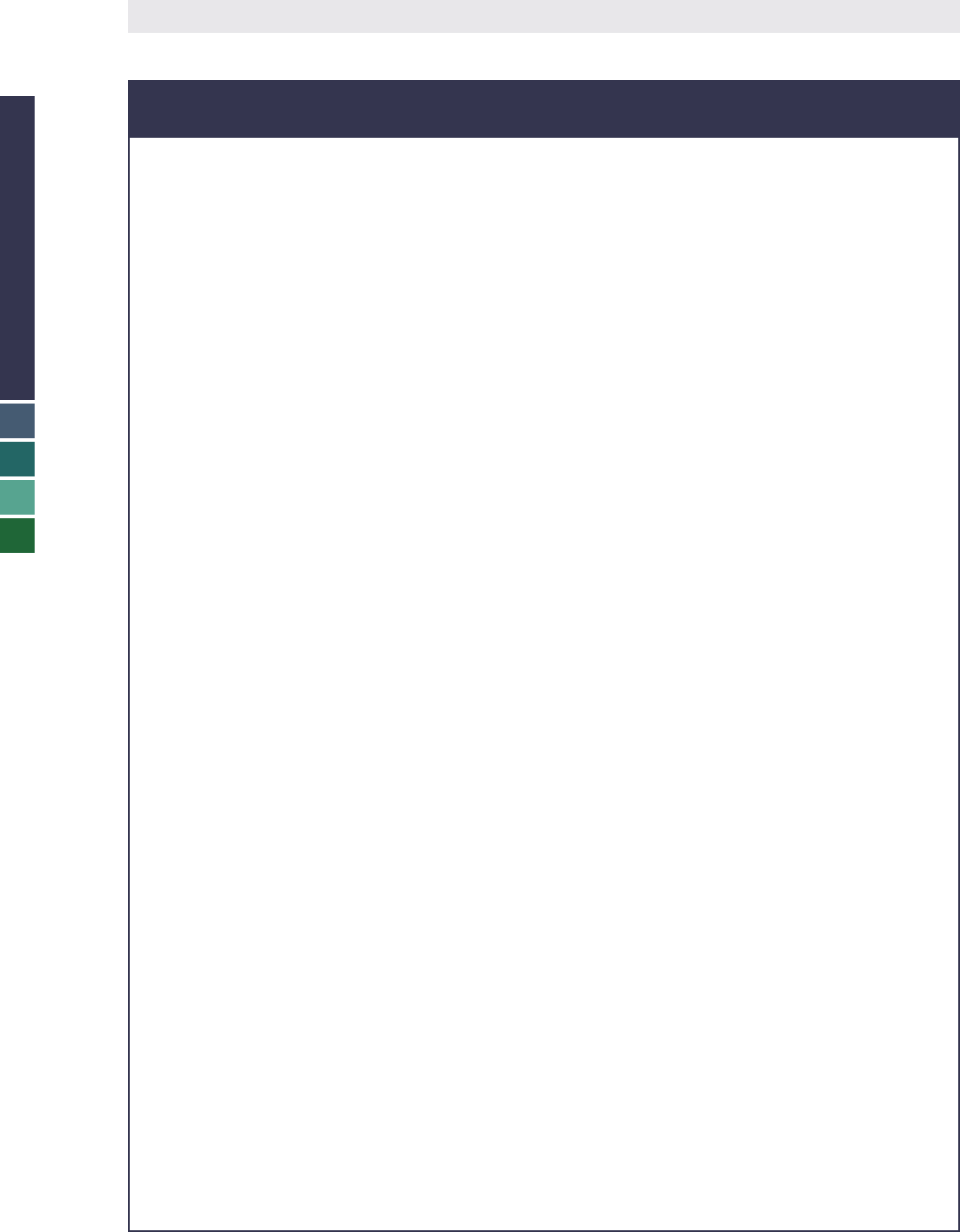

FIGURE 1.3.1, IRS Online Self-Assistance Applications

6

Application

Name

Taxpayer Function

Information

From

Application

Reflected in

Online Account

Type of

Taxpayer

Account

Number of

Transactions

or Sessions,

FY 2019

Number of

Transactions

or Sessions,

FY 2020

Online

Account

make a payment online, request a

or access tax records via Get

Transcript

N/A Individual

Number

unavailable

23,000,000

Get

Transcripts

Online

Retrieve a variety of transcripts

online to view, print, or download

Yes Individual 20,861,000 46,064,000

Get

Transcripts by

Mail

Receive a return or account

Yes

Individual

and

Business

2,545,000 2,156,000

Where’s My

Refund

Learn status of refund No Individual 368,841,000 758,260,000

Where’s My

Amended

Return

No Individual 5,340,000 4,743,000

Direct Pay

Pay directly from bank account Yes Individual 9,420,257 11,841,916

Most Serious Problem #3: Online Records Access

47Annual Report to Congress 2020

Most Serious Problems

Application

Name

Taxpayer Function

Information

From

Application

Reflected in

Online Account

Type of

Taxpayer

Account

Number of

Transactions

or Sessions,

FY 2019

Number of

Transactions

or Sessions,

FY 2020

Online

Payment

Agreements

certain taxpayers

Yes

Individual

and

Business

786,000 844,000

ID Verify

process a federal income tax return

taxpayer identification number

No Individual 132,000 211,000

Get an Identity

Protection

Personal

Identification

Validate identity and retrieve an

Identity Protection PIN online

No Individual

Number

unavailable

488,000

Modernized

Internet

Employer

Identification

Number

Apply for and receive an employer

web

No

Individual

and

Business

4,990,000 6,914,000

Transcript

Delivery

Service –

Reporting

Agents

Retrieve a variety of account

online

No

Individual

and

Business

237,000 374,000

Transcript

Delivery

Service –

States

Retrieve a variety of account

online

No

Individual

and

Business

534,000 604,000

Transcript

Delivery

Service –

Third Parties

Retrieve a variety of account

online

No

Individual

and

Business

104,127,000 108,119,000

Income

Verification

Express

Retrieve transcripts from an online

secure mailbox to verify income of

a borrower

No

Individual

and

Business

14,027,000 16,696,000

Free

Application

for Federal

Student Aid

the Web

Access tax return information and

form

No Individual 18,691,000 27,498,000

Tax

Withholding

Estimator

underpayments

No Individual

Number

unavailable

8,193,000

Interactive

Tax Assistant

Receive answers to basic tax law

questions

No

Individual

and

Business

1,198,000 3,236,000

Most Serious Problem #3: Online Records Access

Taxpayer Advocate Service48

Most Serious Problems

Below we will discuss the challenges taxpayers are facing and why the IRS must upgrade its systems and

provide a robust Online Account for all taxpayers and its employees to assist taxpayers with issues.

Taxpayers Struggle Navigating a Piecemeal System of Online Applications That Have

Limited Capabilities and Incomplete Information

As shown in Figure 1.3.1, taxpayers’ usage of online applications demonstrates their desire to obtain their

information electronically. However, the present system has many downfalls. e IRS has not fully integrated

information and access between online applications and a taxpayer’s Online Account. e information

from the Where’s My Refund tool is not available in a taxpayer’s Online Account, and during 2020, the

information from Get My Payment (Economic Impact Payment) tool was also not incorporated into the

Online Account.

7

Taxpayers wanting to know the date the IRS received and processed their tax returns would

not know which transcript to review, and even then, the transcript may be confusing to a taxpayer. For

example, for taxpayers who filed their return before the due date, the transcript lists the tax return received

date as the due date of the tax return with no explanation. e transcript may list a return posted date that is

later than the date the IRS issued a refund, further confusing the taxpayer. e taxpayer may also have to wait

months after filing a return to see the information in a transcript in the Online Account. Wage and Income

transcripts are not available until mid-May of the processing year.

8

e IRS made some key updates in

September 2020 so that the Online Account immediately shows electronic payments, which means taxpayers

do not have to wait until the payments show up on a transcript to confirm them.

While taxpayers can access some applications through the Online Account, such as Get My Transcript and

the Online Payment Agreement, others such as the Identity Protection PIN are only available outside the

Online Account. Taxpayers using IRS online applications for the first time may face difficulty authenticating

their identities.

9

Some applications have a common login and password; this can actually be a problem for

taxpayers who may have accessed an application years ago and misplaced their login information or perhaps

forgot that they had used another application.

10

Another issue is that each application is limited in what taxpayers can accomplish. For instance, the Online

Payment Agreement is limited to individual taxpayers whose tax debts are below $50,000 ($100,000 if

requesting a full pay agreement)

11

and business taxpayers with a balance of $25,000 or less.

12

Taxpayers

seeking an installment agreement outside of the IRS’s streamline criteria must mail or fax in their request

forms rather than using an online application. Similarly, taxpayers seeking an offer in compromise can use the

IRS’s online Offer in Compromise Pre-Qualifier tool to learn if they qualify but then cannot submit the offer

online; rather, they must mail or fax in the forms.

13

infra

.

10

11

12

13

Most Serious Problem #3: Online Records Access

49Annual Report to Congress 2020

Most Serious Problems

Taxpayers cannot access all the information they need through an online application. For example, the

transcripts available through the Get My Transcript application do not provide the taxpayer with the actual

tax return information, which a taxpayer might need to verify which child he or she claimed as a dependent

on a return. e only way for the taxpayer to view a copy of the actual return filed is to mail a request to

the IRS, pay a $43 fee, and wait up to 75 days.

14

Additionally, it can take up to five months after filing a

tax return for the transcript viewable in the Online Account to reflect the return information.

15

Many of

the IRS’s electronic applications are not available to business taxpayers, including Where’s My Refund, Get

Transcript Online, and the Online Account.

Some of the online applications only provide information temporarily, lacking the capability for the taxpayer

to view the information later. An example is the employer identification number (EIN) application, which

allows taxpayers to apply for an EIN online and receive it immediately once approved. e IRS warns that

once it provides the EIN confirmation notice, it can never regenerate the notice, even if the taxpayer needs

a copy to show proof of the EIN, so taxpayers should save a copy.

16

Taxpayers who need to verify their

information to file a return must call the IRS if they have lost a copy of the EIN notice.

e IRS created the online application, Where’s My Refund, which provides basic information such as an

acknowledgement that the IRS received the tax return. However, for some taxpayers, the application only

supplies a reference code and an IRS phone number, requiring them to call to learn basic information such as

if the IRS applied their refund to an outstanding balance due for another tax period.

17

When the IRS holds

a taxpayer’s refund and asks the taxpayer to verify identity, income, or withholding, the taxpayer must wait to

receive a notice in the mail rather than having the ability to be notified or respond online. Once the taxpayer

submits a response, he or she does not know if the IRS received the response or is processing the refund until

he or she receives another paper notice or the refund itself. From January 1 through October 2, 2019, the IRS

took more than four weeks to release taxpayer refunds it held for potential non-identity theft refund fraud.

18

With an integrated Online Account system, these taxpayers could access further information about the

status of their refunds, submit inquiries about their account, or provide the required information. Security,

uniformity, and ease of use are key to successful online applications, including a robust Online Account.

14

15

June.

16

17

further assistance.”

18

Security, uniformity, and ease of use are key to successful online

applications, including a robust Online Account.

Most Serious Problem #3: Online Records Access

Taxpayer Advocate Service50

Most Serious Problems

Taxpayers Have an Urgent Need for Full Access to Their Information in the Online

Account Now

Although the IRS is working on several initiatives related to the Online Account, taxpayers cannot afford to

wait years for these changes. In FYs 2021-2022, the IRS plans the following actions:

• Expanded Online Account: Taxpayers will be able to make a payment, and certain taxpayers can create

a short-term payment plan within their Online Account.

• Tax Professional Account: Tax professionals and taxpayers will be able to establish digital authorizations

(Form 8821, Tax Information Authorization) and Power of Attorney (Form 2848, Power of Attorney

and Declaration of Representative) with eSignature.

• Secure Document Exchange: More individuals and large and small businesses will have expanded access

to secure messaging and file sharing.

• Authentication: Some digital self-service applications will have new, more secure ways to authenticate,

meeting governmentwide digital identity guidelines.

• Expand Digital Notifications: Taxpayers will be able to view electronic (PDF) copies of additional

notices not previously available in the Online Account and opt-out of paper delivery for some notices.

• Digital Signatures: Authenticated taxpayers and representatives will be able to electronically sign and

submit certain forms and documents.

19

In FYs 2023-2025, the IRS plans to further expand the Online Account by allowing taxpayers to update

contact information and use secure two-way messaging.

20

e IRS introduced new functionalities in its Online Account that allow taxpayers to view a few specific

notices and navigate to a message center.

21

It also plans to implement a feature to alert taxpayers to new

notices. ese are positive steps, but they fall short of what taxpayers need right now. As of late 2020, only

six notices are available in the Online Account, with another five planned for mid-2021.

22

Of the notices

chosen, most are purely informational notices about adjustments or other past actions. e IRS should

instead prioritize notices that provide statutory rights and deadlines to act, such as the statutory notice of

deficiency, providing an opportunity to challenge the liability in U.S. Tax Court; the math error notice,

providing the taxpayer 60 days to request an abatement; and the Collection Due Process (CDP) hearing

notice, providing 30 days to request a CDP hearing.

23

During FYs 2017-2019, the IRS received an average

of 6,745 delinquent CDP hearing requests each year.

24

Placing important notices with deadlines to exercise

taxpayer rights in the Online Account could make it easier for taxpayers to keep track of the deadlines and

19

20

Id

.

21

22

23

See

24

Most Serious Problem #3: Online Records Access

51Annual Report to Congress 2020

Most Serious Problems

exercise their rights. Although the IRS has set a target for placing more notices in the Online Account during

FY 2022, it does not have a definitive plan for how many notices it will be adding to the Online Account,

when it will add them, and how they will be prioritized.

25

e IRS has beneficial elements planned for the Online Account, including the ability to select language

preference for future notices, change the taxpayer’s address, and view alerts that new notices have been posted

within the taxpayer’s Online Account.

26

However, the IRS could do more to notify taxpayers about the

status of their accounts. While the Online Account already includes certain notifications at the top, they are

primarily broader public service style messages one might find on IRS.gov, such as the availability of disaster

assistance or a reminder to file a return if the taxpayer has not done so.

27

ere are only a few notifications

specific to the taxpayer, such as if the taxpayer is in jeopardy of a lien or levy or if a short term payment plan is

past due.

28

e IRS could be tailoring more notifications to specific taxpayer situations, such as if the taxpayer

had a deadline to provide documentation in an examination case.

e IRS is also planning future capabilities for its online application related to POA authorizations, the

Tax Professional Account. By the third quarter of FY 2022, the IRS plans to allow users to view and cancel

pending requests, view and print confirmation of a submission, view and resubmit incomplete requests

due to system error, and save data entries across sessions.

29

Further, the IRS plans to give taxpayers and tax

professionals the ability to view and print authorizations by the third quarter of FY 2023. While positive,

these developments are still years away. To support representatives and taxpayers, the IRS must prioritize an

online application for representatives that allows them to view tax information for their clients for the years

they hold an authorization. Without this access, representatives must rely on paper mail, or they may ask

taxpayers to give them access to their personal Online Accounts, potentially jeopardizing the taxpayer’s privacy

and security. e IRS states it has no plans for the Tax Professional Account to include external notifications,

which slows down the ability for representatives to help clients since clients may not know when a document

needs a signature or when the IRS has processed an authorization.

Unfortunately, there are several Online Account features not planned, such as the ability for taxpayers to view

images of their past tax returns and information returns filed by third parties; file documents and request

actions (e.g., request a CDP hearing, field assignment, or Appeals hearing); view IRS employee contact

information for any open Examination, Collection, or Appeals action; and view the status of compliance

interactions (e.g., the IRS received documentation and the examiner is reviewing).

Additional Complexities Due to COVID-19

e pandemic and resulting impact on taxpayers emphasized the urgent need for a robust Online Account.

During the pandemic, the IRS took the unprecedented step to protect the health and safety of its employees,

their families, taxpayers, and local communities by shutting down some of its operations for months,

including notice printing sites. e IRS had already digitally created many notices and placed them in the

printing queue. Months passed, and when the IRS printed and mailed the notices, they still reflected the

25

26

Id

.

27

Id

.

28

29

Most Serious Problem #3: Online Records Access

Taxpayer Advocate Service52

Most Serious Problems

original dates, including due dates. Taxpayers’ accounts of record reflected the original date on the notices,

not the later date when the notices were mailed.

e total backlog, meaning all notices that were created but were not able to be printed and sent out on

the date appearing on the notice, was approximately 31.2 million notices.

30

However, when addressing

this backlog, the IRS did not treat all notices similarly, leading to taxpayer confusion. We anticipate future

challenges as taxpayers and the IRS work through the different notice scenarios:

• e IRS purged approximately 12.3 million notices and never sent them, but they may still appear on

the taxpayer’s account of record;

31

• e IRS purged approximately 543,000 notices, regenerated them with new dates, and later sent them

out;

32

• e IRS sent approximately 1.8 million notices with original dates on the notice that were prior

(sometimes by months) to when they were mailed, but included an insert explaining that the taxpayer

had additional time to take an action;

33

• e IRS sent approximately 38,000 notices with original dates on the notice prior to when they were

mailed, and taxpayers received a subsequent notice explaining they had additional time to take an action,

but the subsequent notice failed to include a copy of the original notice;

34

and

• e IRS sent approximately 18 million notices with original dates on the notice prior to when they were

mailed but included no insert or subsequent notice providing an explanation.

35

Despite the IRS’s efforts to prioritize which backlogged notices it should mail first, which notices were

statutorily required, and which notices had incorrect dates and required an explanation or new deadline, the

lack of transparency and communication created a situation confusing for IRS employees, taxpayers, and

representatives, impairing their ability to effectively comply and increasing levels of stress. For example, some

taxpayers may have received no communication from the IRS for months during the COVID-19 emergency

when they had a balance due with interest accruing. is was due to the IRS purging certain balance due

notices and then not recreating and mailing them for approximately six months.

36

Conversely, for notices that

were not purged but sent out as generated when the printing sites reopened, some taxpayers received demands

for payment even when they had already made a payment.

37

An Online Account would have allowed the IRS to electronically post the notices and create an alert

informing taxpayers to help mitigate the confusion. Taxpayers who received a backdated CDP hearing notice

may have been especially confused, as some received an insert with their notices providing one date to request

30

31

Id

.

32

Id

.

33

Id

34

refund disallowance.

35

36

37

AX N TODAY

Most Serious Problem #3: Online Records Access

53Annual Report to Congress 2020

Most Serious Problems

a hearing,

38

while other taxpayers later received an additional notice providing a different date to request a

hearing. Viewing copies of these notices online would help taxpayers confirm whether their notice provided

the first revised deadline or the second. Although the situation is understandable, it is unacceptable for the

IRS to issue almost 20 million notices that create confusion and uncertainty.

39

Another area where a robust Online Account would have mitigated problems with the COVID-19 emergency

is incoming mail from taxpayers. During June 2020, the IRS had a backlog of 12.3 million pieces of

unopened mail,

40

with 5.3 million remaining in early October 2020.

41

Taxpayers’ paper refund returns and

identity theft documentation supporting the validity of the refunds sat unopened and unprocessed.

e IRS provided for “digital transmission” of Form 1139, Corporation Application for Tentative Refund, and

1045, Application for Tentative Refund, which allow taxpayers to claim quick refunds (tentative allowances)

for prior year minimum tax liability and net operating loss deductions pursuant to the Coronavirus Aid,

Relief, and Economic Security (CARES) legislation.

42

Still, the “digital transmission” did not mean taxpayers

could submit forms online; rather, they were merely given the option to fax in their forms. Having a portion

of the Online Account where taxpayers could file key forms or requests would have provided an additional

resource for taxpayers to quickly receive their tax benefits provided in the pandemic relief legislation rather

than deal with delays and uncertainty.

Greater Taxpayer Access to Online Records Will Also Benefit the IRS and TAS

e IRS expects to save millions of dollars in postage and printing by placing taxpayer notices in Online

Accounts.

43

Placing additional information about the status of taxpayers’ accounts could reduce customer

service representative time as fewer taxpayers would need to call in to learn about the status of their case in

examination or collection, confirm whether the IRS received and processed a document, or discover which

power of attorneys are on file for which tax years. Online Accounts could free up valuable customer service

representatives for taxpayers who can only use the telephone or mail to contact the IRS. During FY 2019,

the Wage and Investment exam line received over one million taxpayer calls.

44

A survey of taxpayers who

underwent correspondence examinations revealed that over 40 percent called the correspondence toll-free line

simply to check the status of their audit with the majority calling more than once.

45

Some taxpayers reported

calling solely to inform the IRS they had sent the requested documentation.

If the IRS posted notices in the Online Account and provided a notification page where taxpayers could see

what information the IRS is requesting and the related due dates, taxpayers may provide the information

38

39

40

41

42

See

43

44

45

Most Serious Problem #3: Online Records Access

Taxpayer Advocate Service54

Most Serious Problems

more quickly, potentially resulting in shorter cycle times for examinations and collection cases.

46

Finally,

placing information online such as past tax returns, information returns filed by the third parties, and clear

due dates for filing forms and making payments will likely result in fewer taxpayer errors and a greater number

of taxpayers meeting their filing and payment obligations on time.

47

Because the U.S. tax system is built on

voluntary compliance, the IRS benefits greatly from providing top quality service and increasing trust with

tax administration, leading to more taxpayers meeting their tax obligations on their own and reducing the

need for compliance actions. e IRS recognizes the need to expand secure digital options for taxpayers and

professionals to interact efficiently with the IRS while maintaining and improving traditional service options

but has lacked the IT funding to move forward with the speed and accuracy required by taxpayers.

48

TAS receives many cases each year related to IRS delays. During FYs 2018-2019, TAS received approximately

a quarter of its cases under criteria five or six, meaning the taxpayer experienced a delay of more than 30 days

after the IRS’s promised deadline to resolve a tax account problem or had not received a response or resolution

to the problem or inquiry by the date promised.

49

Viewing the status of a case in examination, appeals,

collection, or another part of the IRS would keep taxpayers informed about where their case stood and may

mitigate the need for a TAS case. TAS works with the IRS to provide taxpayers with copies of IRS notices.

Placing all notices online would allow TAS to focus more on obtaining relief for the taxpayer without the

added time and burden of establishing the paper trail between the taxpayer and the IRS.

CONCLUSION AND RECOMMENDATIONS

Although the IRS has taken positive steps and plans to expand online applications to provide greater access

to information, there still remains a large gap between the IRS’s offerings and the robust online experience

taxpayers need and a quality tax administration requires. e COVID-19 emergency highlighted the

46

20

47

48

49

See

Because the U.S. tax system is built on voluntary compliance, the

IRS benefits greatly from providing top quality service and

increasing trust with tax administration, leading to more

taxpayers meeting their tax obligations on their own and

reducing the need for compliance actions.

Most Serious Problem #3: Online Records Access

55Annual Report to Congress 2020

Most Serious Problems

downfalls of relying on paper. Although the IRS has contemplated many improvements to the Online

Account, the National Taxpayer Advocate recommends expediting the completion date of improvements

such as integrating a case management system, providing business taxpayers with full access to the same

information individual taxpayers have within the Online Account, and integrating secure messaging and

document upload capabilities. Without additional funding, the IRS cannot timely expand its Online

Account, which requires taxpayers to rely on the phone and mail for their tax records, resulting in taxpayer

burden and harm.

Preliminary Administrative Recommendations to the IRS

e National Taxpayer Advocate preliminarily recommends that the IRS:

1. Provide business taxpayers access to Online Accounts.

2. Prioritize posting to the Online Account notices that provide the taxpayer with statutory or

administrative rights, a deadline for action, or notice of a potential intrusive enforcement action, such

as levy.

3. Develop a timeline for when all remaining notices used by the IRS, outside the 11 notices already

scheduled, will be available to be viewed within taxpayers’ Online Accounts.

4. Update the programming for the Online Account application so taxpayers can view available notices

that were issued prior to when the taxpayer signed up for the Online Account.

5. Provide access to all self-assistance online applications through the Online Account.

6. Update and consolidate Online Account information to reflect information from all other IRS online

applications.

7. Integrate secure messaging so that taxpayers can initiate and view messages and upload and download

documents to and from the IRS within their Online Accounts.

8. Place taxpayer-specific alerts and notifications on the main dashboard of taxpayers’ Online Accounts to

notify them of the status of their cases and specific deadlines for action.

9. Allow taxpayers to add, change, or remove authorized representatives through the Online Account.

10. Allow taxpayers to give authorized representatives access to Online Account records for the authorized

tax years.

11. Allow taxpayers to update their address and other contact information through the Online Account.

12. Allow taxpayers to make certain requests and file certain forms through the Online Account, such as a

CDP request, a penalty abatement request, or a tentative carryback application for refund where e-file

is not otherwise available.

Legislative Recommendations to Congress

e National Taxpayer Advocate recommends that Congress:

1. Continue to fund the technological upgrades the IRS requires to provide an enhanced level of service

that the country deserves to improve its overall operations.

2. Provide sufficient funding for the Business Systems Modernization account to enable the IRS to

replace its 1960s technology systems, create an integrated case management system, and offer robust

Online Accounts for taxpayers and practitioners.

50

50

(

).

Most Serious Problem #3: Online Records Access

Taxpayer Advocate Service56

Most Serious Problems

IRS COMMENTS

We agree with the National Taxpayer Advocate on the need for robust online services as one part of

our omni-channel approach to customer service consisting of internet capabilities, correspondence,

telephone, and face-to-face interactions. We have focused for several years now on prioritizing,

building and delivering the services that are most needed, while also considering feasibility given

significant resource and technology constraints. e IRS systematically reviews taxpayer and

stakeholder feedback, market research, and strategic priorities to inform our product prioritization

and development.

Since launching Online Account for individual taxpayers in 2016, the IRS has added many new

features using an agile development process with releases approximately every nine weeks. e IRS

has a long list of ideas and must continuously prioritize which features to work on with the available

capacity, taking into consideration the taxpayer and business benefit and the level of effort. e

team has prioritized features that don’t otherwise exist online, or where there were opportunities for

significant user experience improvements. Current features available to individual taxpayers via their

Online Account include personalized messaging on the home page with reminders to file, lien or

levy status, payment plan details and status, and any pending payments. Additionally, in November

we added a Message Center where taxpayers can view and download digital copies of six high

priority notices. ese notices cover 23% of the notice volume sent by the IRS, totaling more than

26 million notices, and taxpayers can view through Online Account any of these notices issued since

November 15, 2020. In January we plan to display a taxpayer’s Economic Impact Payment amount

in Online Account, providing a digital way to look this up when filing 2020 tax returns for taxpayers

who have misplaced or have not received the related notices and need to claim additional amounts.

In accordance with the Taxpayer First Act (TFA), the IRS recently developed a 10-year strategy for

improving the taxpayer experience. is strategy will help drive prioritization and decision making

going forward. e TFA Taxpayer Experience Strategy includes plans to further expand on existing

Online Account features and add new ones. However, any future expansion or acceleration would be

dependent on receipt of funding.

In Fiscal Year (FY) 2021, the IRS plans to add additional notices, show the taxpayer’s address on file,

enable taxpayers to sign tax professional authorizations, and offer the option to create a short-term

payment plan in Online Account. In partnership with the Bureau of the Fiscal Service, the IRS plans

to enable taxpayers in FY 2022 to make payments through Online Account, allowing taxpayers to

view their balance and pay it in a single session online without having to reenter information, better

enabling voluntary compliance and improving the user experience. In FYs 2022-2024, the IRS plans

to add the option to update contact information, allow opt-in and -out of paper notices, allow access

to secure messaging in Online Account, and add additional features for tax professionals.

We appreciate the National Taxpayer Advocate’s support for additional and consistent funding for

digital modernization and the National Taxpayer Advocate’s recognition of the positive steps the IRS

has taken to expand online services for taxpayers. e IRS is committed to high-quality, seamless

Most Serious Problem #3: Online Records Access

57Annual Report to Congress 2020

Most Serious Problems

experience — through expanded digital service options as well as through improved traditional

channels — in order to help resolve diverse taxpayer needs and promote voluntary tax compliance.

TAXPAYER ADVOCATE SERVICE COMMENTS

TAS appreciates that the IRS is forward-thinking in regard to providing taxpayers comprehensive

access to their online records through the Online Account and other applications. As discussed in

the Most Serious Problem and the IRS response, there are many future features the IRS is planning

that will greatly benefit taxpayers. Providing business taxpayers with the same access to online records

as individual taxpayers will be critical to ensuring all taxpayers can easily access the information they

need to comply with their tax obligations.

roughout the Most Serious Problem, we illustrate problems with relying on a piecemeal system

of online applications, where taxpayers must use one application to find some information and

then another application to find additional information or take an action. e IRS has made some

progress in integrating applications. e IRS’s future plans to allow taxpayers to view a balance

and pay it in a single session will encourage taxpayer compliance and reduce taxpayer frustration.

Another step forward is the plan to make information regarding Economic Impact Payments available

in the Online Account starting in early 2021. However, the IRS has not committed to integrating

all its taxpayer-facing online applications into the Online Account. is step is key to making access

to online records simpler for taxpayers. Although the IRS states that it is prioritizing features that do

not otherwise exist online, it should also make adjustments to existing features so they are easier to

use and integrated in one place.

e Most Serious Problem discusses the downfalls of relying primarily on transcripts to inform

taxpayers about their accounts. As explained, the transcript can be confusing to taxpayers, who

cannot easily ascertain from the transcript when a return was filed or when a refund was issued.

Additionally, the transcript lacks key information shown on a taxpayer’s return, such as the

dependents claimed for certain tax benefits. e IRS has not committed to posting actual copies

of returns within the Online Account, and we hope this is something it will reconsider in the near

future.

TAS is pleased to learn the IRS has already begun posting notices in the Online Account, starting

with the six notices that were part of a November 2020 update. e IRS indicates that the notices

chosen represent a significant portion of all notices the IRS sends. While it is positive that the IRS

is focusing on posting high-volume taxpayer notices in the Online Account, TAS believes the IRS

should not only consider volume but also the impact on taxpayer rights when it chooses which

notices to include next. Many of the notices included or planned are primarily informational notices.

Missing from the list of notices currently available or planned for FY 2021 are some key taxpayer

Most Serious Problem #3: Online Records Access

Taxpayer Advocate Service58

Most Serious Problems

notices such as the statutory notice of deficiency, which provides a taxpayer’s only opportunity to

challenge a liability in court prior to paying it; the CDP notice, which offers the taxpayer a deadline

to request a hearing before the IRS Independent Office of Appeals; and the refund disallowance

notice, which sets a two-year deadline to challenge a refund disallowance. TAS encourages the IRS to

develop a prioritization plan for posting notices that considers the impact on taxpayer rights as well as

volume.

e IRS must accelerate its timeframe for posting additional notices in the Online Account.

e 31.2 million notices created during mid-2020 that could not be mailed on time due to the

COVID-19 pandemic demonstrate how it is crucial for taxpayers to have access to their notices

online. As taxpayers are grappling to understand the impact of the late-mailed or purged notices

and what it means for their account balances and due dates, the IRS can leverage the Online

Account to provide information. For example, even if a taxpayer lost a copy of his or her refund

disallowance notice, and this notice is not yet included in the Online Account, the IRS could use

personalized messaging to provide an alert to the taxpayer regarding when his or her deadlines expire

for administratively appealing the disallowance or challenging it in court. e Most Serious Problem

gives examples of other personalized status updates.

Overall, the IRS has made great strides toward providing more taxpayer information online. TAS

understands that funding will continue to dictate when and what improvements the IRS can make to

online services. Notwithstanding this restriction, TAS believes the following recommendations will

help the IRS prioritize changes that will make it simpler for taxpayers to access their tax information

online and will promote taxpayer rights.

RECOMMENDATIONS

Administrative Recommendations to the IRS

e National Taxpayer Advocate recommends that the IRS:

1. Provide business taxpayers access to an online account similar to the IRS’s Online Account

that is available to individual taxpayers.

2. Prioritize posting to the Online Account notices that provide the taxpayer with key statutory

or administrative rights, a deadline for action, or notice of a potential intrusive enforcement

action, such as levy.

3. Develop a timeline for when all remaining notices used by the IRS, outside the 11 notices

already scheduled, will be available to be viewed within taxpayers’ Online Accounts.

4. Provide access to all self-assistance online applications through the Online Account.

5. Update and consolidate Online Account information to reflect information from all other IRS

online applications.

6. Integrate secure messaging so that taxpayers can initiate and view messages and upload and

download documents to and from the IRS within their Online Accounts.

7. Place taxpayer-specific alert banners on the main dashboard of taxpayers’ Online Accounts to

provide information regarding their status of their cases and highlight important deadlines,

Most Serious Problem #3: Online Records Access

59Annual Report to Congress 2020

Most Serious Problems

such as the due date for providing documentation in an examination, the assignment of a

balance due case to a Revenue Officer, or the deadline to request a CDP hearing.

8. Allow taxpayers to add, change, or remove authorized representatives through the Online

Account.

9. Allow taxpayers to give authorized representatives access to Online Account records for the

authorized tax years.

10. Allow taxpayers to update their address and other contact information through the Online

Account.

11. Allow taxpayers to make certain requests and file certain forms through the Online Account,

such as a CDP request, a penalty abatement request, or a tentative carryback application for

refund where e-file is not otherwise available.

Legislative Recommendations to Congress

e National Taxpayer Advocate recommends that Congress:

1. Continue to fund the technological upgrades the IRS requires to provide an enhanced level of

service that the country deserves to improve its overall operations.

2. Provide sufficient funding for the Business Systems Modernization account to enable the IRS

to replace its 1960s technology systems, create an integrated case management system, and

offer robust online accounts for taxpayers and practitioners.

51

51

(

).