TravelManual

PoliciesandProceduresforfaculty/staffregardingpaymentfor

travelexpensesincurredforUNCGreensboro.

Publishedby: OfficeoftheController

Revised: April14,2021

Page|0

TableofContents

TravelOverview...................................................................................................................Page1

ForeignNationalVisitors/Non‐ResidentAliens....................................................................Page2

RequiredAuthorizations......................................................................................................Page3

TravelAdvanceLoans...........................................................................................................Page4

Transportation.....................................................................................................................Page5

Subsistence..........................................................................................................................Page9

Third‐PartyLodging............................................................................................................Page12

RegistrationFees................................................................................................................Page12

EntertainmentReimbursements........................................................................................Page13

Non‐EmployeeReimbursements.......................................................................................Page13

InternalConferences..........................................................................................................Page15

ExternalConferences.........................................................................................................Page16

InternationalTravel............................................................................................................Page18

TravelTips..........................................................................................................................Page18

TravelTerms......................................................................................................................Page21

CompletingTRV‐1Form.....................................................................................................Page21

FrequentlyAskedQuestions..............................................................................................Page27

References.........................................................................................................................Page27

Page|1

Travel‐Overview

Purpose/Scope

TheTravelManualprovidesbasicinformationontravelpoliciesandprocedures.Themanualis

based onTheStateBudgetManual, Section 5, which sets forth travel policies and regulations

relativetosecuringauthorizationandreimbursementofexpendituresforofficialstatetravel.The

administrationandcontroloftravelisinaccordancewiththeprovisions ofGeneralStatutes(G.S.)

138‐5, 138‐6, and 138‐7.The University must also comply with IRS Publication 463 Travel,

Entertainment,Gift,andCarExpenses.

Thepoliciesand proceduresasstatedinthismanualapplytoStateBudgetedFundsdeposited

withtheStateTreasurer, whetherderived fromappropriationsoragencyreceipt;Institutional

TrustFunds,includingDiscretionaryandOverheadReceiptFunds;andContractsandGrants.

Policy

Allowable travel expenses will be reimbursed to authorized University personnel and other

individualstravelingonofficialstatebusiness.Alltraveliscontingentuponavailabilityoffunds.

ThepoliciesandproceduressetforthinthismanualappliestoallUniversityofNorthCarolinaat

Greensborofaculty,staff,students,andotherindividualswhotravelonbehalfoftheUniversity.

Before travel expenditures are incurred, all travelers and administrative personnel should be

awareofthetravelpoliciesandproceduresstatedinthismanual. Pleaserefertravelquestions

toAccountsPayable(336)334‐5798oremailattravel@uncg.edu.

OfficialStateBusiness:OfficialstatebusinessoccurswhentheStateemployeeorotherpersonis

traveling to attend approved job related training, work on behalf of, officially represent, or

provideastateserviceupontheState’sorUniversity’srequest.

§5.0.3

Travelthatdoesnotdirectly

benefittheStateandtheUniversitywillnotbereimbursable.

EmployeeResponsibility:Beforetravelingtheindividualmustread,understand,andabidebythe

policiesandproceduressetforthinthismanual.Priorapprovalauthorizationforovernighttravel

is delegated to the traveler’s supervisor. Travelers must complete the Travel Authorization

portionoftheFormTRV‐1priortoovernighttravel.Employeestravelingonstatebusinessare

responsible for submitting reimbursement requests in accordance with UNCG policies. The

employeewhoistravelingonofficialstatebusinessfortheUniversityisexpectedtoexercisethe

samecareinincurringexpensesthataprudent personwould exerciseif travelingonpersonal

business and expending personal funds. Excess costs, circuitous routes, delays, luxury

accommodations and services unnecessary,unjustified, or for the convenience or personal

preferenceoftheemployeeintheperformanceofofficial businessarenotacceptableunderthis

Page|2

standard.

§5.0.2

Travelerswillbe responsibleforunauthorizedcostsandanyadditionalexpenses

incurredforpersonalpreferenceorconvenience.

Traveler’s Supervisor Responsibility:Approval authorization for travel is delegated to the

traveler's supervisor. This individual's approval indicates that appropriate review of the cash

advance/reimbursementhasbeenmade,andthetravelconformstoallrulesandregulationsand

isproperlysupportedwithvaliddocumentationandreceipts.

Timely Submission: Travel reimbursement requests should be submitted complete and with

proper funding to Accounts Payable within 30 days of the return date.

NCGS §138‐6(c)

Per IRS

accountable plan guidelines, any travel reimbursement requests received in Accounts Payable

sixty(60)daysorlaterafterthereturndatewillbetaxabletothetraveler.

IRS§62(c);Treas.Reg.§1.62(c)(2)

Travel expense reimbursement requests that are not received complete, with proper

documentation,andfundingwithin60daysofthereturndateofthetravelwillbeconsidered

taxableincometothetraveler.Asapplicable,ifthetravelerisanemployee,thereimbursement

willbereportedontheemployee’spayandrelatedW2,orifthetravelerisanon‐employee,the

amount will be reported on 1099‐MISC. It is the responsibility of the funding department to

ensurethatfundswillbeavailableinadvanceofauthorizingarequestfortravel.Fundingchanges

and/ordelayshavenobearingontherequiredtimelysubmissionand/orpotentialemployeetax

liabilityfordelayintimelysubmission.

ForeignNationalVisitors/Non‐ResidentAliens

Foreignnationalvisitors/non‐residentaliensmaybeemployeesoftheUniversity,aswellasnon‐

employees.Dependentupontheirspecificcircumstances,theirvisatype,andpurposeoftravel

as it relates to their purpose of visiting the US/UNCG, the following may apply: 1) the travel

expenditureisallowedwithouttaxwithholding,2)thetravelexpenditureisallowed,butrequires

tax withholding, or 3) the travel expenditure/reimbursement is not allowed.Only holders of

certainvisatypesareeligibletoreceivetravelreimbursementsorbenefitfromUniversity paid

travel.Foreignnationalvisitors/non‐residentaliensaresubjecttowithholdingoftaxesontravel

reimbursement, including payment to a third party in their behalf, unless an exemption is

providedbytheIRSCodeoranincometaxtreaty.Toreduceoreliminatetaxwithholdingonthe

reimbursement,ataxtreatymustbeineffectbetweentheUSandtheindividual’staxresidence

country.CallthePayrollTaxManagerat(336)334‐5180oremailat[email protected]fordetails

concerningeligiblevisatypesandtaxtreaties.Requestfortaxwithholdingexemptioninvolves

submittingthetraveler’sIRSForm8233tothePayrollOffice,821S.JosephineSt.,forforwarding

totheInternalRevenueService.(ThePayrollOfficewillassistwithpreparingtheForm8233.)IRS

regulationsrequireholdingofreimbursementpaymentsfortendaysaftertheformismailedto

theIRS.Inordertoavoiddelaysintravelreimbursementtonon‐residentaliens,FormNRA‐001

withrequireddocumentsisneededtoassistinpreparingtheForm8233andshouldbereceived

inthePayrollOffice two(2)weeksprior to thedatetravelreimbursement isexpected.Ifit is

Page|3

determined,withinthePayrollOfficethatanindividualisentitledtoatravelbenefit,thecontents

ofthisTravelManualareapplicable.

PleaserefertotheForeignNationalVisitorTaxGuideandapplicableNRAformsforclarification.

RequiredAuthorizations

TravelbyseniorUniversityadministrators,exceptforin‐statedaytravel,requiresauthorization

asfollows:

Travel by the Chancellor shall be authorized by the Vice Chancellor for Finance and

Administration.

Travel by Vice Chancellors and others who report directly to the Chancellor shall be

approvedbytheChancellororapersondesignatedtodosobytheChancellor.

TravelbyDeansandotherswho reportdirectlytotheProvost/ExecutiveViceChancellor

shallbeauthorizedbytheProvost/ExecutiveViceChancellororapersondesignatedto

dosobytheProvost/ExecutiveViceChancellor.

Individuals who are designated to approve travel shall ensure that an alternate approver is

availableincaseswheretheprincipalapproverisunavailable.

SeniorUniversityAdministratorsaredefinedas:

ChancelloranddirectreportstotheChancellor,

Deans,

MembersoftheExecutiveStaffwhoreportdirectlyto the Provost

ForemployeeswhoarenotdesignatedasaseniorUniversityadministrator,departmentheads,

orcomparableadministratorshavebeengiventhisdelegation.

AlltravelfundedbyContactsandGrantsrequirespriorapprovalfromthe OfficeofContractand

GrantAccounting.

Itistheresponsibility ofthefundingdepartmenttoensurethatfundswillbeavailableinadvance

ofauthorizingarequestfortravel,regardlessofwhetherovernightorsamedaytravel.

Rubberstamps,digitalstamps,oracopyofasignaturewillnotbeaccepted.Allsignaturesmust

beoriginal.SeeCompletingTRV‐1Formsectiononhowtoproperlysubmitatravelauthorization.

Page|4

TravelAdvanceLoans

TravelAdvanceLoansareonlyavailableunderthefollowingcircumstances:

Studentgrouptravel

Athleticteamtravel

BlanketAthletictravel

BlanketAdmissionstravel

Researchoverseasforanextendedperiodoftime

TravelexpensesthatareunabletobepaidviathePcard

Advancesarenotavailabletonon‐employees.

Theadvancerequestcannotbelessthanonehundreddollars($100)orgreaterthantheestimatedcost

oftravel.

A travel advance loan is a loan to the employee; therefore, it is the responsibility of the

employee to ensure that the advance is either repaid or cleared by submitting Travel

Authorization/ExpenseReport(FormTRV‐1)andrepayinganyunusedadvancemonies.Failure

torepaythetraveladvance loanwithinthirty(30)daysofthe returndatemayleadtopayroll

deductionoftheadvanceamountfromtheemployee’snextpayrollcheck.Ifapayrolldeduction

ismadefromanemployee’spayrollchecktorepayatraveladvanceloan,the employeeforfeits

the right to participate in the Travel Advance Loan program and will no longer be eligible to

receivetraveladvanceloans.

AdvanceRequest

Atraveladvanceloanmustberequestedona TravelAuthorization/ExpenseReport,FormTRV‐

1,whichmustbesubmittedtotheController’sOffice atleasttwo(2)weekspriortointended

travel.OntheformthereisasectionontherightunderneaththeTravelAuthorizationsection

fortherequestedfundandamountoftheadvanceloan.Youwill notneedtoputanythingon

theTRV1formatthistime.Acopy shouldbesenttoAccountsPayableandtheoriginalshould

remainwiththetraveleruntilcompletionofthetrip.TheoriginalTV1formshouldbesubmitted

withthereceiptswithin30daysofthereturntrip.

BlanketTravelAdvanceLoan

ForAthleticandAdmissionsemployeeswhotraveleachmonth,anannualadvanceoffundsmay

beissuedequaltoonemonth’saverage monthlyexpense.Eachmonth,areimbursementrequest

willbefiledforpaymentforexpensesincurredthepreviousmonth.Theblanketadvancemust

be repaid as of June 20 annually. If it is determined that the monthly reimbursement has

averaged less than the annual advancement, the advance must be reduced to the newly

establishedamount.

Page|5

IssuanceofTravelAdvanceLoan

Theadvancemaybeissuednosoonerthanfive(5)calendardayspriortotravel.

SecondTravelAdvanceLoan

A second travel advance loan can be made only if the traveler has submitted a Travel

Authorization/ExpenseReport(FormTRV‐1),coveringthefirstadvance. Nomorethantwo(2)

traveladvanceloanscanbeoutstandingtoanytraveleratanyonetime.

RepaymentofTravelAdvanceLoans

Within thirty (30) days following the completion ofthe travel, a Travel Authorization/Expense

Report (Form TRV‐1) for travel expenses must be submitted to the Accounts Payable or the

advance must be repaid. Any unused monies from the advance must also be promptly paid.

Travel advance loan repayments should be made by check payable to UNCG.DO NOT SEND

CASH.Ifareimbursementrequestformisnotfiledwithinthirty(30)daysaftercompletionof

travel,theentireadvanceamountwillbedeductedfromtheemployee’snextpayrollcheck.Ifa

payrolldeduction ismadefromanemployee’spayrollchecktorepayatraveladvanceloan,the

employeeforfeitstherightto participateinthetraveladvanceloanprogramandwillnolonger

beeligibletoreceivecashadvances.

TripDelayorCancellation

Ifatraveladvanceloanisobtainedandthetripisnottaken,theadvancemustberepaidwithin

forty‐eight (48) hours of cancellation or if the original check has not been cashed, it may be

returnedtotheController’sOfficetobevoided.Ifthetripispostponed,theadvance mustbe

repaidandanewadvance obtainedagainst anewTravelAuthorization/ExpenseReport,Form

TRV‐1.

Transportation

AirTransportation

Confirmation of airfare travel or an itinerary cannot be used as proof of payment; an

airfare receipt must be attached showing the payment method and identifying

informationsuchasnameand/orlastfourdigitsofcreditcard.

Aircoachisareimbursableexpense,butfirstclassisnotareimbursableexpense,except

in rare cases in which a written justification is submitted in advance of the trip and

approved.

Page|6

Reimbursementforfeesforcheck‐in,seatassignments,andbaggageislimitedtoactual

costssubstantiatedbyreceipt.

Flightinsuranceisnotareimbursableexpense.

Familymembers’airfareisnotareimbursableexpense.

Iftheairfarereceipthasmorethanonenameonit,theonerequesting

reimbursement

mustprovideproofoftheindividualrequestedamount.

Iftheflighthasdelaysandresultsinalongerstay,anexplanationmustbeprovided.

Change fees and cancelled reservations must have a written statement providing a

businessreasontobereimbursed.

Frequentflyermilesearnedbya stateemployeewhiletravelingonstatebusinessatstate

expensearethepropertyofthestate.

With sufficient justification and documentation and with approval of the department

head,stateemployeescanbereimbursedforusual,customary,andreasonablefeesand

services charges imposed by the travel agency for assistance in making travel

arrangements.

§5.2.24

AirportParking

Airportparkingwillonlybereimbursedforstatebusinesstravel.

Anyparkingratesconsideredexcessiveandonlyfortheconvenienceofthetraveler

are not reimbursable.For example, use of an airport’s hourly parking lot for an

overnighttripwouldbeconsideredexcessive.

Inappropriateorillegalparkingthatresultsinacitationwillnotbereimbursed.

Anoriginalreceiptshowingamountanddatesisrequiredforreimbursement.

Parkingchargesareenteredonthe“other”lineontheFormTRV‐1andmustbenoted

alongwithanyothermiscellaneousexpensesonthesecondpageofthetravelform.

The business standard mileage rate set by the Internal Revenue Services for a

maximumoftworoundtripswithnoparkingcharge,oroneroundtripwithparking

chargesisreimbursable.Receiptsarerequiredforairportparkingclaims.

§5.2.26

CharteredAircraft

Theuseofcharteraircraftmustbeapprovedbythedepartmentheadorhis/herdesignee,

providedthefollowingissubstantiatedandputinwriting:

Astateaircraftisnotavailableornotappropriateforthesizeofthepartytravelingor

thedestinationairport.

Theuseofacharterflightismoreeconomicalthanacommercialflight.

Theuseofacharterflightisnecessarybecauseofunusualtravelcircumstances.

Page|7

PriortothetripthetravelermustsubmitaFormTRV‐1formwithcompletewritten

justification for utilizing a charter flight and must have authorized signatures

approvingtherequest.

Bus/Railtransportation

Travelermusthavetheoriginalbus/railreceiptstoobtainreimbursement.Ifreceipts

arenotavailable,acredit

cardstatementshowingtheamountpaidmaybeprovided.

Ifacreditcardstatementisused,theremustbeidentifyinginformationincludedon

thestatement,suchasthetraveler’snamesothatthestatementcanbeverifiedas

belongingtothetraveler.

Railroadmusthaveareceiptat“CoachFareRate”.

RentalCar

Itistheintentofthestatethatstateemployeetravelshall beconductedinthemost

efficientmannerandatthelowestandmostreasonablecosttothestate.Rentinga

carisoftentheleastexpensiveoption.Forbothin‐stateandout‐of‐statetravel,rental

vehiclesshallbeobtainedthroughthestate’stermcontractswhenavailable.

§5.2.13

The

StateofNorthCarolina,andaccordinglyUNCG,havestatecontractrentalagreements

withEnterprise,Hertz,andNationalCarRental.Additionalinformationislocatedat

https://purchasing.uncg.edu/policies section 4.2State TermContracts.NCGeneral

Statute§116‐13allowspurchasesfromotherthanthestatetermcontractprovided:

theitemis“substantiallysimilar”tothatonstatecontract,andthecostislessthan

statecontract.

EnterpriserentalcarscanbeobtainedthroughUNCGParkingOperationsandCampus

AccessManagement.

Anitemizedreceiptmustbeprovided;therentalcaragreementwillnotsufficeasa

receipt.

No reimbursement for rental car insurance will be made because state employees

traveling on official state business are covered under the state’s auto insurance

program. Additional insurance information is located at rsk.uncg.edu/vehicle‐

insurance‐information‐certificates‐forms/.Rentalcarinsuranceisincludedwithinthe

categoryof“HiredandNon‐Owned”vehicles.

Ifthetravelinvolvesanypersonaltraveltime,therentalcaramount mustbeadjusted.

PersonalVehicle

Itistheintentofthestatethatstateemployeetravelshall beconductedinthemost

efficient manner and at the lowest and most reasonable cost to the state. With

regardstopassengervehicletravel,whetherin‐orout‐of‐state,agencytravelpolicies

shall:

Page|8

Maximize utilization of state‐owned vehicles (agency‐owned or agency‐assigned

vehiclesownedbytheDepartmentofAdministration)

Makeuseofstatetermcontracts for short‐term rentals(StateTermContract975B

VehicleRentalServices),and

Reimburseforuseofpersonalvehiclesonalimitedbasis.

§5.1.26

When state‐owned vehicles are not available, employees may procure vehicles

throughthestate’stermcontractsorbereimbursedthroughuseofpersonalvehicles.

Business use of personal vehicles are reimbursable based upon actual mileage.

Mileage is measured from the closer of duty station or point of departure to

destination(andreturn).

EmployeesshallbereimbursedthebusinessstandardmileageratesetbytheInternal

RevenueService(56centspermileeffectiveApril1,2021)whenusingtheirpersonal

vehicleforstatebusiness.

Parkingfees,tolls,andstoragefeesarereimbursablewhentherequiredreceiptsare

obtained. Fines for traffic and parking violations are the responsibility of the state

employee.

Ifthetravelerchoosestodriveratherthanflywhentravelingout‐of‐state,anairfare

comparison must be attached showing the mileage is the economical option. The

airfarecomparisonshouldhavethesamedaysofthetravel.

DocumenteddrivingdistancessuchasprovidedbyGoogleDirections, MapQuest,etc.

mustbeattachedtotheFormTRV‐1formrequestingreimbursement.

IftherearemultipledaysofmileageforasingleFormTRV‐1,theremustbeatravel

logattachedshowing:traveler’sdeparturedate;descriptionoftravel,destinationand

mileageforeachdaytraveled.

Themileageiscalculatedfromthetraveler’sdutystationorhomewhicheverisclosest

and the returntrip.Ifany extramileageoccurs there must be written justification

submittedwiththeFormTRV‐1.

Ifthetravelerleavesonaweekendfromtheirhome,mileageisstillcalculatedfrom

dutystationorhomewhicheverisclosest.

Mileagefromdutystationtotheemployee’shomeisnotreimbursable.Thisincludes

employeeswhoareon“callback”status(seeStateHumanResourcesManual).

Extramileageaccumulatedfornon‐essentialtravelisnotreimbursable.

Taxi

Taxi,carservice,mobilephoneorderedcarservice,orairportshuttlefarestothehotel

from the airport and from the hotel to the airport will be reimbursed with a valid

receipt. Use of Public Transportation‐In lieu of using ataxi or airport shuttle, etc.

employeescanbereimbursedwithoutareceiptforupto$5eachone‐waytripeither

fromtheairporttothehotelormeetingplaceandorfromthehotel,meetingplace

totheairport.Thetravelerhastheoptionofbeingreimbursedfortheactualcostof

thetravelwiththesubmissionofanoriginalreceipt.

§5.2.26

Page|9

Ifthetraveleris usingataxi,car service,ormobileordered carservicetogo home

fromtheairportorfromhometotheairportawrittenexplanationmustbeprovided.

Theremustbeadateonthereceiptthatiswithinthedaterangeofthetrip.

Theactualcostsofthesefaresarereimbursablewhenrequiredfortravelonofficial

state business. The request must be documented with a receipt. The use of public

transportationisreimbursableforactualcostswithareceipt.

§5.2.26

Tips for taxi or car service, etc. must be no more than $5 per taxi or car service

trip.

§5.2.26

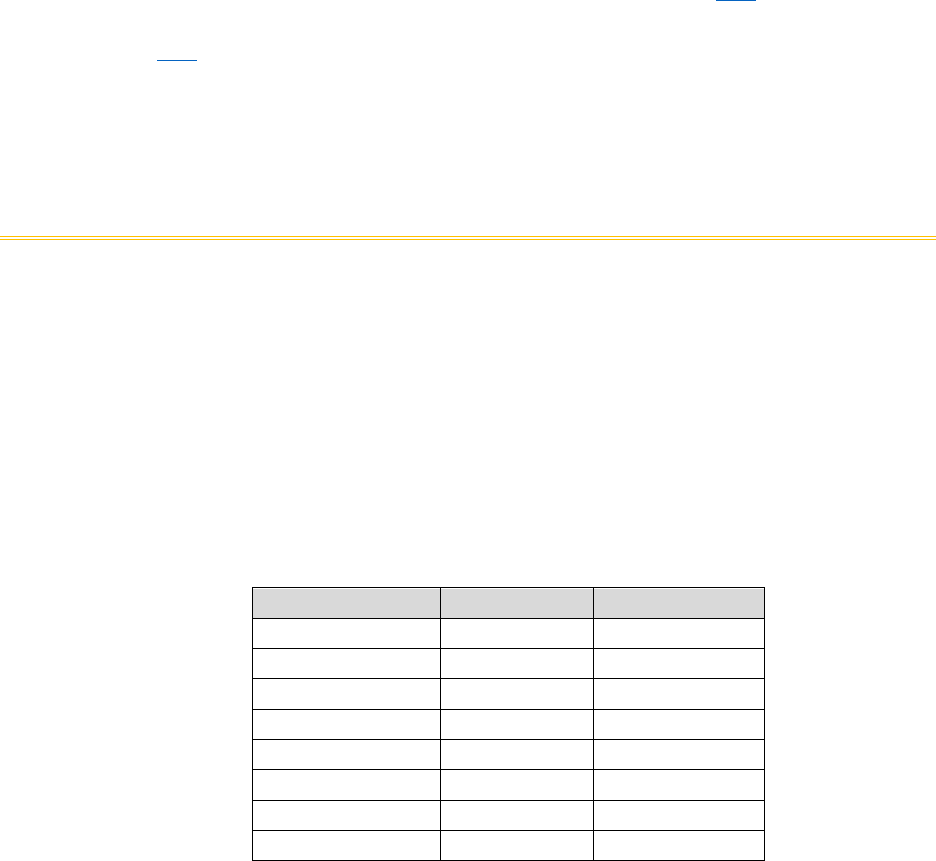

Subsistence

Astate employeemaybereimbursedformeals,includinglunches,whileonofficialstatebusiness

whentheemployeeisinovernighttravelstatus.Employeesreceiveallowancesformealsand

lodging for full days of travel.Employees and other qualified travelers also qualify for

allowances/subsistence rates when using hotel and meal facilities located in North Carolina

immediatelypriortoandreturningfromoutof state travel during the same travel period. An

explanationoftheallowancesthatcanbe claimedforeachcircumstancearedetailedbelow:

RateofAllowances

Meals In‐State Out‐of‐State

Breakfast $8.60 $8.60

Lunch 11.30 11.30

Dinner 19.50 22.20

Total $39.40 $42.10

Lodging $75.10 $88.70

24‐HourPeriod $114.50 $130.80

(Revised7/1/19effectiveforthe2019‐21biennium.)

Twenty‐four(24)HourPeriod–FullDay

Atwenty‐four(24)hourperiodisdefinedasthetimebetween12:01a.m.and12:00p.m.

midnight.Itissynonymouswiththecalendarday.

To obtain reimbursement for lodging, an itemized receipt of actual expenses from a

commercial lodging establishment or an online travel site must accompany the travel

reimbursement request. The receipt must indicate check in/check out dates.

Page|10

Reimbursement for lodging may only be made in the amount documented by lodging

receipts.

Toqualifyforreimbursementforlodgingforovernightstays,thetraveldestinationmust

be located at least thirty‐five (35) miles from the employee’s regularly assigned duty

stationorhomewhicheverisless.

Out‐of‐statetravelstatusbeginsthedaytheemployeeleavestheStateandremainsin

effectthroughtheday theemployeereturnstotheState.Accordingly,in‐stateallowances

andreimbursementratesapplywhenemployeesandotherqualified officialtravelersuse

hotel and meal facilities located in North Carolina immediately prior to leaving North

Carolinaandreturningfromout‐of‐state.

Please see Third Party Lodging section of this manual for lodging other than hotel or

motel.

LessThanATwenty‐four(24)HourPeriod–PartialDay

Allowances will be paid for meals for partial days of travel when the partial day is the day of

departure or the dayofreturnportion of the overnighttravel. The following table details the

requirementstoclaimsuchreimbursement.

Meal DayofDeparture DayofReturn Comments

Breakfast Leavebefore6:00

a.m.

N/A Mustextendthe

workday2hours

Lunch Leavebefore12

noon

Returnafter2:00

p.m.

Cannotbeclaimed

unlesseitherthetrip

requiresan

overnightstayorthe

costofthelunchis

partofaregistration

fee

Dinner

Leavebefore5:00

p.m.

Returnafter8:00

p.m.

Mustextendthe

workdayby3hours

Whentravelinga partialday,thetimeofdepartureand/orreturnmustbenotedonthe

RequestforReimbursementofTravelandOtherExpenseswhenfilingforreimbursement.

Excesslodgingauthorizationforin‐state,out‐of‐state,andout‐of‐countrytravelmustbe

obtainedinadvance.Excesslodgingmayberequestedbecausetheavailablelodging is

Page|11

more expensive than the state allowable amount. Excess lodging authorization is not

allowed for reason of convenience or personal preference. Supervisory personnel

certifying the reimbursement request as necessary and proper must require

documentation from the traveler to substantiate that the overnight lodging was

necessary.TheStandardStateSubsistenceratecanbeadministeredtotravelthatdoes

notreceivepriorapproval.

Thetravelmustinvolveatraveldestinationlocatedatleast35milesfromtheemployee’s

dutystationorhomewhicheverislesstoreceivereimbursement.Dutystationisdefined

as the location where the employee is regularly assigned. The designation of an

employee’shomeasthedutystationrequirestheapprovalofthedepartmenthead.

Thehotelreservationdatesmustbewithinonecalendardayofthepurposeoftravel.

Thetravelreimbursementshallbefiledwithinthirty(30)daysafterthetravelperiodends

by submitting an original, itemized, paid hotel invoice along with a Form TRV‐1, and

includingalltheappropriatesignaturesauthorizingapproval.

If the lodging receipt has someone else’s name on it other than the one requesting

reimbursement, or if the room was shared and there are two different credit card

numbersonthefolio,theremustbeproofattachedmatchingthetraveler’srequestfor

reimbursement.

§5.3.2

Allowancesformealsshallnotexceedthestate‐determinedrateforsubsistence.

Theamountoftipsareincludedinthetotalofthemealallowance.

§5.2.10

Departureandarrivaltimesmustbelistedonthereimbursementrequest.

Mealsincludedinotherrelatedactivities,suchasregistrationfeesandconferenceagenda

mustnotbeduplicatedasasubsistencereimbursementrequest.

An employee may be reimbursed, if requested, for breakfast even if their lodging

establishmentoffersafreecontinentalbreakfast.Receiptsarenotrequiredformealsthat

willbeclaimedatstatesubsistencerates.

§5.2.10

Meals/RegistrationFee

Registration fees may be paid by the department or the employee. When a registration fee

includesthecostofone(1)ormoremeals,itistheresponsibilityofthedepartmenttoensure

thatreimbursementsforsuchmealsarenotmadetotheemployeeinadditiontotheregistration

fee.The cost of any meals included in the registration fee must not be included in the

reimbursementclaimsforregistration.Ifaconferencehasamealthatanemployeewishesto

be reimbursed and is not included in the price of registration, a business reason must justify

reimbursementforthatmeali.e.,roundtablemeeting/lunch,awardluncheonwherethetraveler

isgettinganaward,etc.

MealsandDay‐to‐DayActivities

Stateemployeesmaynotbereimbursedformealsinconjunctionwithacongress,conference,

assembly, convocation or meeting, or by whatever name called, of employees within a single

statedepartment,institution,university,oragency,orbetweenemployeesoftwoormorestate

Page|12

departments,institutions, universities,oragenciestodiscussissuesrelatingtotheemployee’s

normalday‐to‐daybusinessactivities.

§5.2.8

ThirdPartyLodging

University sanctioned travel may occasionally stipulate the use of lodging in an apartment or

home rather than a hotel or motel upon documentation that per day lodging rates provide

savingstotheState.Thispolicywasdevelopedasaninternalmethodofauthorizingthirdparty

lodgingforanyonetravelingonofficialUniversitybusiness.

When requesting to use third party lodging that exceeds State lodging rates, an appropriate

comparisonoflocalhotelsmaybesubmittedasevidenceofsavingstotheUniversity.Thirdparty

lodging agreements are not allowed among family members or where such agreements or

payments create a financial conflict of interest to the traveling employee or other university

managers or employees. Any requests that do not show a savings must provide sufficient

justification to support the necessity for third party lodging. Each applicant must provide a

completedPre‐ApprovalThird PartyLodgingform(TRV‐TPL)anda signed rentalagreement to

the University Controller prior to the trip before approval may be granted for payment or

reimbursement.PriortoforwardingtoAccountsPayableeachrequestmustbeapprovedbythe

DepartmentHeadortheDepartmentHead’sdesignee.

ThefollowingprovidersshouldnotbeconsideredasThirdPartyLodging:Orbitz.com,Hotel.com,

Travelocity.com,Airbnb.com,orotheruniversities.

RegistrationFees

State employees may be reimbursed for the actual amount of conference registration fees as

shownbyavalidreceiptorinvoice.Registrationfeesaretypicallychargedtoallowanemployee

toparticipateinaconference,andthefeesarecollectedtodefraythecostofspeakers,building

(room) use, handout materials, breaks and lunches. Registration fees are distinguished from

tuitionfeesandshouldbereimbursedonaFormTRV‐1.

ToursandSocialEvents

Thecostsofoptionaltours,entertainment(plays,sportingevents,etc.),andsocialactivitiesare

notreimbursableand,ifincludedintheregistrationfee,mustbesubtracted.

Page|13

SubstantiationandReimbursementofRegistrationFees

Whenrequestingpaymentofregistrationfeeseitherinadvanceorafterthetripiscompleted,a

copyofbrochures,feeschedules,conferenceagenda,orothermateriallistingtheamountand

various elements of cost included in the registration fee should be attached to the Travel

Authorization/ExpenseReport(FormTRV‐1).Torequestreimbursementforregistrationfees,a

validreceiptorinvoicemustbeprovidedwithTravelAuthorization/ExpenseReport(FormTRV‐

1).

EntertainmentReimbursements

Entertainmentexpensesassociatedwiththetravelbeingreimbursedshouldbeonthe

FormTRV‐1andnotonaBANFIN‐32,DirectPayAuthorization.

Atravelercanonlybereimbursedforentertainmentifheorshehastakenothersoutfor

businesspurposes.

Anofficialstatebusinessreasonmustbestatedfortheentertainment.

Alistofindividualswhowerepresentmustbeincludedwiththeoriginalitemizedreceipt.

Statefundscannotbeusedforentertainment,pleasefillintheappropriatefundnumber

intheentertainmentbox.

“Entertainment‐Fund Holder’s Initials” must be filled in by the fund holder who is

authorizedonthefundbeingchargedfortheentertainment.

Appropriate original, itemized receipts must be attached tothe Form TRV‐1 to receive

reimbursementforentertainment.

Formoreinformationaboutentertainmentpleasegoto:FinancePolicy8.

Non‐EmployeeTravelReimbursements

Students

Allstudentswhoareintravelstatusaresubjectto thesametravelandsubsistencepoliciesthat

applytootherUniversityemployees.Studenttravelexpensescanonlybepaidorreimbursedif

thestudentison“officialstatebusiness”thatprimarilybenefitstheuniversity.Travelfor“official

statebusiness”forstudentsisdocumentedthroughthecompletionoftheTRV‐SStudentNon‐

EmployeeTravelAgreementform.

Student employee travel expenses can be paid from state funds if the student is traveling on

behalfof theirpositionandthe positionis fundedbystatefunds.Studenttravelexpensescan

also be paid from state funds, if approved in advance by the Dean or their designee, in the

followingcircumstances:

Page|14

Thestudenttravelisforthepurposeoffulfilling acourserequirement(coursenumber

mustbespecified),

The student travel is for the purpose of serving as the official representative of the

Universityforanevent,

Thestudenttravelisforthepurposeofpresentingataconference

thatprimarilybenefits

theuniversity,ratherthanthestudent.

Non‐employee student travel must be paid from the appropriate funds supporting that

purpose/activity. Travel by students for the purpose of participating in activities of student

organizationsorathleticcontestsmustbepaidfromnon‐statefundssupportingthatparticular

organizationoractivity.

AcompletedStudent Non‐EmployeeTravel Agreement(FormTRV‐S) shouldbeapprovedin

advanceofthetravelbytheDepartmentHead/Dean/Director,andattachedtoeachTRV‐1or

BANFIN‐32 form(ifapplicable)fortravelpertaining to individual students. . The TRV‐S form

providesdocumentationthatthetravelmeetsthecriteriaof“Universitybusiness”asindicated

ontheform.Studenttravelthatdoesnotmeetthe“Universitybusiness”criteriawillbetreated

astaxableincometothestudentandreportedonIRSform1099.

Forstudentgrouptravel,ofwhichnoreimbursementisbeingmadetoanystudents,alistofthe

participatingstudentsmustbe providedwiththeTRV‐1usedtodocumenttheexpendituresfor

thetravelevent.ThelistofstudentsshouldindicateifanyofthestudentsareclassifiedasNon

ResidentAliens(NRA)sothattheirtravelcanbeprocessedinaccordancewithIRSregulations.A

TRV‐Sformforeachindividualstudentisnotrequiredforgrouptravelinwhichstudentsarenot

beingreimbursedfortravelexpenses.Examplesofthistypeofgrouptravelinclude;athleticteam

travel,servicelearningopportunities,clubsports,andfacultyledstudyabroadtrips.

Non‐StateEmployees

Non‐stateemployeestravelingonstatebusinesswhose expensesarepaidorreimbursedbythe

State of North Carolina are subject to these regulations, including statutory subsistence

allowances,tothesameextentasarestateemployees.Travelexpensesformembersofanon‐

employee’sfamilyarenotreimbursable.Non‐employeesarenoteligiblefortraveladvances.

ProspectiveProfessionalEmployees

Department Heads or comparable supervisors are authorized to approve reimbursement of

transportation expenses of prospective professional employees for employment interviews.

Theseexpensesarelimitedto transportationandsubsistenceforthree(3)days(or5daysifone

ofthedaysisaSaturday)atthein‐staterate.

§6.4.1

Page|15

AttendantsforHandicappedEmployees

State policy does not permit the routine payment of salaries for attendants who are assisting

handicapped employees. Payment of subsistence expenses (lodging and meal costs) for

attendantsmaybereimbursedifadvanceapprovalisobtainedfromtheDepartmentHeadwhen

anattendantisneededduetoanovernightstayawayfromhomeonofficialstatebusiness.

InternalConferences

InternalConferences

Internal Conferences are those that involve participation of employees within a particular

department, institution, or agency only. No payment for meals is allowable unless overnight

travelcriteriaaremet.

CriteriaforAuthorizedInternalConferences

Theconferenceisplannedindetailinadvance,withaformalagendaorcurriculum.

Writteninvitationto participants, settingforththe calendarofeventsandthedetailed

scheduleofcost

No excess travel subsistence may be granted for internal departmental meetings,

conferences, seminars, etc., and such meetings must be held in state facilities when

available.

Noregistrationfeemaybecharged.

§7.4

Sponsoringdepartmentsmayprovide refreshmentsfor“coffeebreaks”providedthere

aretenormoreparticipantsandcostsdonotexceedfivedollars$5.00perparticipant.

§7.4

A department cannot use state funds to provide promotional or gift items to be

distributedattheconference.

A department cannot use state funds to support or underwrite a rally, celebration, or

similarfunction.

A department cannot use state funds to support or underwrite a meeting, assembly,

conference, seminar, or similar function by whatever name called that promotes any

causeorpurposeotherthanthemissionandobjectiveofthedepartment.

Page|16

ExternalConferences

ExternalConferences

External conferencesare those that involve the active participationofpersons other than the

employeesofasinglestatedepartment,institution,oragency.

Wheneverfeasible,conferencesshouldbeheldinfacilitiesownedbystatedepartments.When

necessary, non‐state facilities may be rented and the cost charged to account code 238210 –

conferenceroomrentalwithoutallocationtoparticipants’dailysubsistenceallowances.

§7.3

AuthorizedExternalConferences

Conferencessponsoredorco‐sponsoredbyastatedepartmentareconsideredauthorizedwhen

theymeetthefollowingrequirements:

Thereareasubstantialnumberofparticipants,withatleasttwenty‐five(25%)percentof

theparticipantscomingfromoutsidethelocalarea.

Theconferenceisplannedindetailinadvance,withaformalagendaorcurriculum.

Thereisawritteninvitationtoparticipants, settingforththecalendarofevents,thesocial

activities,ifany,andthedetailedscheduleofcosts.

RegistrationFees

Registrationfeesmaynotincludecostsofentertainment,alcoholicbeverages,setups,or

flowers.

Tours, entertainment, and social activities are not reimbursable and should not be

includedinregistrationreimbursement.

Traveler must provide an itemized, original receipt showing traveler’s name, amount,

andpaymentmethod.Acreditcardstatementonlyshowingthenameofconferenceand

amountdoesnotprovideenoughinformation.

Registration fees exceeding thirty dollars $30 may be charged by the sponsoring

departmenttoparticipantsforcostsofexternalconferences.

Aconferenceagenda,brochure,orothersupportingdocumentationshouldbeattached

totheFormTRV‐1toprovideinformationabouttheevent.

Meals

Iftheconferenceinvoiceseparatesthecost of the mealfromtheregistrationamount,

themealwillnotbereimbursedandperdiemwillbeapplied.

Ifthetravelerisrequestingreimbursementforamealinadditiontoandnotincludedin

registration,theremustbeevidencethatattendanceatthismealwasmandatory.

Page|17

RefreshmentsatAssemblies

Sponsoringdepartmentsmayproviderefreshmentsfor“breaks”providedthereareten(10)or

moreparticipantsandcostsdonotexceedfivedollars$5.00perparticipantperparticipantper

day.

§7.3

BudgetedExternalConferences

When conferences are to be held under the sponsorship of a state department in which the

funding for all participants is budgeted, lump‐sum payments to a conference center or an

organization may be made upon written authorization from the Department Head. The

authorizationmustprovide:

Purposeanddurationoftheconference,

Numberofpersonsexpectedtoattend,

Specificmealstobeservedattheconference;(Paymentformealscanonlybemadewhen

such conference involves the active participation of persons other than the state

employeesandmustbenecessaryforconductingofficialStatebusiness),

Approximatedailysubsistencecostperperson,

Name of the conference center, hotel, caterer, or other organization providing the

service.

Payment will be made only when sponsoring departments provide the following

documentations:

Anitemizedinvoiceshowingtheapprovalofthedepartmenthead,and

Alistofnamesandaffiliationsofthoseattending.

Itistheresponsibilityofthedepartmenttoensurethatreimbursementformealsincludedinthe

lump‐sum payment is not also included in reimbursement payments made to conference

participants.

InternationalTravel

AFormTRV‐1isfilledoutwithpriorapprovalandappropriatesignaturesforanyout‐of‐country

travel,consistentwithanytravel,ifitinvolvesanovernightstay.Priorapprovalauthorizationfor

overnighttravelisdelegatedtothetraveler’ssupervisororauthorizedpersonnel.Iftheemployee

orotherqualifiedofficialtravelersusehotelandmealfacilitieslocatedoutside ofNorthCarolina,

butwithinthecontinentalUS,immediatelypriortoanduponreturningfromoutofcountrytravel

butduringthesametravelperiod,outofstate subsistence ratesshallapply.

Page|18

All foreign travel funded by contract or grant funds requires prior approval of the Office of

ContractandGrantAccounting.FederalcontractsandgrantsrequiretheuseofUSFlagcarriers

unlessotherwiseapprovedbythesponsoringagency.

Inadvanceofforeigntravel, tobetter ensurecompliancewithfederallaws,eachtraveler that

travelsinternationallyshouldrefertoUNCGExportControls.

Employees may elect to claim the subsistence rate* for meals plus incidental travel expenses

(M&IE)publishedbytheDepartmentofStateforanyforeigntravelfundedbyafederalagency

onacontractorgrantfund.Thisdecisionmustbemade priortosubmittingtheproposaltothe

fundingagencyandtheappropriatefederalperdiemrequestedintheproposedbudget.

Foreigntravelchargedtostatefundsortrustfundsmayuseeitherstateratesforsubsistenceor

thefederalperdiemdependingontheavailabilityoffundsandsubjecttothepriorapprovalof

thesupervisorandauthorizedfundholder.

Ifanemployeeelectsto claimthefederalperdiem,regardlessoffundingsource,thepublished

perdiemisthemaximumamountthatcanbereimbursed.ExcessSubsistenceforLodgingwill

notbeallowed.Areceiptoflodgingexpensesfromacommerciallodgingestablishmentmust

bepresentedforreimbursement.

IfthecurrencyisotherthanUSDaprintoutshowingthecurrencyconversionforthedatesused

mustaccompanythetraveltosubstantiatethecurrencyconversion.Documentationmayinclude

abank/currencyexchangereceiptwhichreflectstheinitialcurrencyexchangeplusadministrative

feestoarriveatthenetcurrencyexchange.OANDA.comisaweb‐sitethatcanbeutilizedto

showmatchingconvertedcurrencyamountsalongwiththeappropriatedateofdisbursement.

*International rates for meals plus incidental travel expenses (M&IE) are available on the US

DepartmentofStatewebsite.

TravelTips

FormTRV‐1TravelPreparation

Travelplansinvolvinganovernightstayortraveladvancemustbeapprovedinadvance

ofthetripbyhavingthetopportion(TravelAuthorization)oftheTRV‐1formfilledout

completely and signed by the traveler (left top) and Supervisor/Dean (right top).

SignaturesmustbedatedBEFOREthetrip.

Alltravelreimbursements(TRV‐1)shouldbesubmittedtoAccountsPayablenolaterthan

30daysfromreturndateoftravel.Travelreimbursements(TRV‐1)receivedafter60days

fromdateofreturnwillbetaxedperIRSguidelines.

Page|19

Rubberstamps,digitalstamps,oracopyofasignaturewillnotbeaccepted,allsignatures

mustbeoriginal.

Plan ahead and allow at least seven (7) business days for travel to be audited and

reimbursed.

AllgrantfundedtravelmustbesenttoContractandGrantAccountingforapprovalbefore

submittedtoAccountsPayable.

Non‐employeestudent travelrequiresa TRV‐SformalongwithaTRV‐1 form.Students

thatareemployeesdonotneedtocompleteaTRV‐Sform.

Obtain original receipts and/or corroborating documentation, such as a credit card

statementwithidentifyinginformationforanyandallexpensesthatarebeingrequested

tobereimbursed.Pleasedonottapeoverimportantinformationonthesereceipts,such

asdates,amountsetc.asthiswillerasetheinformation.Theoriginalreceiptshouldshow

thecostofgoodsorservicesprovided;itshouldhavethetravelersnameonitorother

identifyinginformation,andshowthedateandthemethodofpayment.

Anyincompleteinformationwilldelaythereimbursement.

Prepayments/directpaymentstovendors

Vendorprepayments/directpaymentsforairfare,hotelandregistrationare madeinthe

middlesectionoftheFormTRV‐1form“UNCGDirectPaymentstoVendor(s)ThruA/P”.

The PCard may be used to pay some vendors.The list of allowable travel expenses on

PCardislocatedonthePurchasingwebsite.

ATRV‐1shouldbeusedforthesedirectpaymentstoavendor,ratherthanaBANFIN‐32,

sincethecompletionoftheFormTRV‐1“TravelAuthorization”sectionisalsoapplicable.

IfthevendorisnotalreadyintheBannerSystem,pleaseobtainaW‐9fromthe vendor

andsubmitwiththeFormTRV‐1requestingpayment.

This section must have the fund number, authorized initials, amount of payment, and

accountnumbercompleted.

WhenpayingavendorthebottompartoftheFormTRV‐1andthebottomsignaturesare

notneeded.Thetopsignaturesandtheinitialsforthefundwillbesufficientforpayment.

AttachanoriginalvendorinvoicetotheFormTRV‐1forpaymenttothevendor.

Revisions

Revisionsareonlyallowedwhenafinalizedtripneedstobemodified.Forexample;ifan

additionalreceiptwasfoundafterthefinalreimbursementhadalreadybeensubmitted

andprocessed.

AcopyoftheoriginaltravelreimbursementshouldbesubmittedtotheAccountsPayable,

marked “REVISED” in red and include all original receipts pertaining to the revised

amounts.Allrevisionsmustbeapprovedandincludeappropriateoriginalsignatures.

InternationalTravel

Page|20

Allinternationaltravelchargedtoafundnumberthatstartswith200‐225(grantfunds)

mustbeapprovedbyContractandGrantAccountingbeforesubmittingtotheAccounts

Payable.

Internationaltravelrequiresoriginalreceipts,consistentwithdomestictravel.

IfthecurrencyisanythingotherthanUSD,aprintout

showingthecurrencyconversion

forthedatesusedmustaccompanythetraveltosubstantiatethecurrencyconversion.

Documentationmayincludeabank/currencyexchangereceiptwhichreflectstheinitial

currency exchange plus administrative fees to arrive at the net currency exchange.

OANDA.comisoneweb‐site that can be utilized to showmatchingconvertedcurrency

amountsalongwiththeappropriatedateofdisbursement.

Mealre imbursementforinternationaltravelmaybereimbursedattheout‐of‐staterates

or foreign per diem rates.For out‐of‐state rates, see Subsistence Section of manual.

ForeignperdiemratescanbereviewedontheUSDepartmentoftheStatewebsite.

Reimbursementsforcost‐incurredwhileobtaining orrenewingapassportmaybemade

to an employee who, in the regular course of his or her duties, is required to travel

overseasforofficialstatebusiness.

§5.2.30

Employees traveling internationally on overseas flights may be reimbursed actual

businessclassfare(substantiatedbyreceipt)withpriorapprovalofthedepartmenthead.

DirectDeposit

Allemployeedirectdepositreimbursementswillbedepositedintothetraveler’sbankaccount

accordingtotheirbank’sschedule.

TipsandGratuity

Reimbursable gratuity or tips must be considered reasonable for items that are not already

coveredunderSubsistence.Excessivetipswillnotbereimbursed.Areasonabletipwouldbeone

that a prudent person would give if traveling or conducting personal business and expending

personalfunds.

Forfurtherguidance, the followinginformationisprovided whencalculatinga

tip:

Airports:BaggageHandling/Skycaps=nomorethan$2perbag;

ShuttleDrivers=nomorethan$2perbag

Parking/AutoRelated:Valets=$2percarwhencollectingthecar;

Taxiorcarservicedrivers=nomorethan$5pertaxiorcarservicetrip.

Other

The “other” line on Form TRV‐1 is for parking fees, telephone charges, gas, and other extra

expenses.Airfare baggage fees do not belong on this line.Airfare baggage fees should be

includedintheairfaretotal.

Page|21

TravelTerms

Travel:Allactivitiesinvolvingexpensesfortransportation,subsistence,orregistration,whichare

authorizedtobepaidfromstatefundsand/ornon‐statefunds.

Duty Station: The job locationwhere employee spends the majority of working hours. For an

employeeinatravelstatusthemajorityofthetime,dutystationiseitherhomeoroffice.

StatutoryRate:TheratessetbyNorthCarolinaGeneralStatutes(G.S.)

In‐State:WithinthebordersofNorthCarolina

Out‐of‐State:AlloftheUnitedStatesexceptNorthCarolina,AlaskaandHawaii

Out‐of‐Country:OutsideofthecontinentalUnitedStates

Subsistence:Lodgingandmealswhichincludesgratuities.

StateEmployee:Anyemployee,whethertemporaryorpermanent,whoispaidonastatepayroll.

Non‐Employee:

AconsultantwhosecompensationisnotpaidthroughtheUniversitypayrollsystem.

An employee of another governmental jurisdiction‐local orfederal‐in whose travel the

statemayhaveabusinessinterest.

Aprospectivestateemployee(includesUniversityfacultyorstaff).

AnenrolledstudentatUNCG,notonPayroll,oranenrolledstudentatanotheruniversity

orcollege.

CompletingtheTRV‐1Form

General

TheTRAVELAUTHORIZATION/EXPENSEREPORT,FormTRV‐1,mustbeutilizedbyalluniversity

departments,schools,andofficestoobtainapprovaltotravelandtorequestreimbursementof

travelexpenses.

TheTRV‐1formisavailableontheFinancialServiceswebsite.

Page|22

FormTRV‐1–TravelAuthorization/ExpenseReport

TheTravelAuthorization/ExpenseReportisinitiatedbytravelersconductinguniversity‐related

business.

Iftraveladvanceloanorpaymentstovendorspriortotriparerequiredandthetripinvolvesan

overnightstay,thetravelermustcompletetheTRAVELAUTHORIZATIONsectionoftheform

andobtaintheproperapproval(s)beforethetravelistotakeplace.Retainthissignedform

untilcompletionoftravel.

Ifatraveladvanceloanand/orpaymenttovendorpriortotriparerequiredandthetrip

involvesanovernightstay,thetravelermustcompletetheTRAVELAUTHORIZATIONand

TRAVELADVANCELOAN/PAYMENTTOVENDORPRIORTOTRIPsection.Pleasenotethatsome

registrationsareduewellinadvanceofthebeginningofaconference.Acopyoftheformisto

besenttoAccountsPayableatleast10businessdayspriortotravel,or10businessdaysprior

toanyregistrationdeadline,whicheverisearlier.DonotsendtheoriginalTRV‐1formto

AccountsPayablebeforethetriphasbeencompleted.

TheREIMBURSEMENTOFEXPENSESPAIDBYTRAVELERORCHARGEDTOPCARDsectionmust

becompletedandsubmittedtoAccountsPayablewithin30daysofthereturnfromtrip.

CompletingtheTRAVELAUTHORIZATIONSection:

Allitemsmustbecompletedbythedepartmentliaisonortraveler.

Ifthetravelerisanon‐residentalien,attachNRA001formwithrequireddocumentation.Attach

FormI‐551(greencard)forLegalPermanentResident.

TRAVELER’SNAME:

Thetraveler’sname.

UNIVERSITYI.D.NUMBER:

Thetraveler’sUniversityidentificationnumber.

UNCGEMPLOYEE:

Checkyesifanemployee.

TELEPHONENUMBER:

Fillinthecontactperson’stelephonenumber.

DATEFILED:

Datetravelauthorizationisprepared.

Page|23

ADDRESS:

Ifanemployee,thetraveler’scampusaddress.Ifnotanemployee,the traveler’shomeaddress.

AREYOUASTUDENT?:

Checkapplicablebox.

CITIZENSHIPSTATUS:

Checkapplicablebox.

DESTINATION:

Thetraveler’sdestination.

DESCRIPTION:

Checktheappropriateboxforreasonfortravel.(OfficialStateBusinessoccurswhena

Universityemployeeorotherpersonistravelingtoattendapprovedjobrelatedtraining,work,

onbehalfof,officiallyrepresent,orprovideastateserviceupontheUniversity’srequest.

AcademicCreditandStudentActivityareforstudentuseonly.)Provideabriefexplanationof

thetravel’spurpose.Ifanassociationmeetingorconventionisbeingattended,youmay

abbreviate.

ESTIMATEDCOSTOFTRIP:

Fillinestimatedcostoftripnotexceedingtheexpectedreimbursement.Useworksheeton2

nd

pageofformforassistance.

PERIODCOVEREDBYTHISVOUCHER:

Thebeginandenddatesandtimesoftheproposedtravel.

TRAVELADVANCEDLOAN:

Thissectionneedstobecompletedonlyifthetravelerrequestsatraveladvanceloan.The

traveladvanceloanrequestedcanbenomorethantheestimatedcost,andcanbenolessthan

$100.

EnterFundnumberandadvanceloanamount.

TRAVELER’SSIGNATURE:

Thetraveler’ssignature.

SUPERVISOR’S/DEAN’SSIGNATURE(S):

Thesupervisor’s/dean’ssignatureindicatestheapprovalofthebusinesstravelandanytravel

advances,specificexceptionsrelativetolodging,theuseofapersonalcarorrentalvehicle,

airportparking,andanyotherexceptionsforvalidUniversitybusinesspurposes.SeeRequired

Authorizationsectionofthismanual.

Page|24

CompletingtheUNCGDirectPaymentstoVendor(s)ThruA/PSection:

Thissectionisusedtopayvendorsforairfare,hotel,and/orregistration.Attachtheoriginal

invoicesforpayment.

SendacopyofthepartiallycompletedformtotheController’sOfficeforprocessing.The

originalshouldbekeptinthetraveler’sofficeforcompletionattheendoftravel.

FUNDNUMBERFORPAYMENTSTOVENDORS:

Fillinsix‐digitfundtocharge.Thefundholder’sinitialsmustbebesideeachfundnumberlisted.

andsupervisor’ssignaturemustbeontheSupervisor/Dean’sSignature(s)lineinthe‘Travel

Authorization’section.

AIR:

FillinvendornameandamountofairfarepaidbytheUniversityandattachoriginalinvoice.

Selectappropriateaccountcode.

HOTEL:

FillinvendornameandamountofhotelpaidbytheUniversityandattachoriginalinvoice.

Selectappropriateaccountcode.

REGISTRATION:

FillinvendornameandamountofregistrationpaidbytheUniversityandattachoriginalinvoice

orsupportingdocumentationshowingamountoffee.Selectappropriateaccountcode.

CompletingtheREIMBURSEMENTOFEXPENSESPAIDBYTRAVELER/ORCHARGEDTOPCARD

Section:

Ontheoriginalformwhereauthorizationwasgrantedbycompletionofthe‘Travel

Authorization’section,completethetransportation,subsistence,andotheritemsinthissection

showingactualexpenses.NotethatanyitemspaidbytheUniversitypriortotravelshouldnot

beincludedinthissection.

Any‘other’expensesmusthaveareceiptoranexplanationattachedtotheTRV‐1form.The

supportingexplanationmayalsobewrittenintheboxonthereversesideoftheform.

Entertainmentexpensesclaimedmustincludewhowasentertained,itsbusinesspurpose,and

mustbesupportedbyitemizedreceipts.Entertainmentexpensesmaynotbechargedtoastate

fund(11XXXX).Ifthefundholderissomeoneotherthanthepersonauthorizingthetravel

reimbursement,thepersonauthorizedtosignforthefundbeingusedtoreimburse

entertainmentexpensesmustinitialtheapprovalarea.

Page|25

ReconcileanyamountduetothetravelerortheUniversity.ShowamountsduetheUniversity

inparenthesesandattachacheckinthatamounttothe TRV‐1.Checksshouldbemadepayable

toUNCG.Donotsendcash.

Transportation:

Actualcostforappropriatetransportation.Attachreceiptunlesspaidpriortotripbythe

University.DonotincludeanyamountspaidbytheUniversitypriortotrip.

AIR:

Ifairfareisused,attachreceipt.Costofinsuranceisnotreimbursable.SeeTransportation

sectionofthismanualforrulesconcerningairfare.

BUS/RAIL:

Ifbus/railtransportationisused,attachreceipt.Costofinsuranceisnotreimbursable.See

Transportationsectionofthismanualforrulesconcerningbus/railtransportation.

RENTALCAR/TAXI:

Ifrentalcarisused,attachreceipt.Costofinsuranceisnotreimbursable.SeeTransportation

sectionofthismanualforrulesconcerningcarrental.

MILEAGE:

Ifpersonalvehiclewasused,enterTotalMileageinappropriateratefield.Selectonlyone

mileagerateunlessusingaTravelLog.SeeTransportationsectionofthismanualforcurrent

mileagerates.

Subsistence:

HOTEL:

Actualnumberofnightsatacommerciallodgingestablishment, roomrate(includingtax)per

day,andthetotalamount.Originalreceiptmustbeattached.

MEALS:

Thenumberofbreakfasts,lunches,anddinnersthetravelerclaims,theperdiemamountper

meal,andthetotalamount.SeeSubsistencesectionofthismanualforrulesandperdiemrates

concerningmeals.Mealscannotbeclaimedifincludedinaconferenceregistrationfee.

Other:

REGISTRATION:

Actualcostofregistrationfees.AttachreceiptunlesspaidpriortotripbytheUniversity.Donot

includeanyamountspaidbytheUniversitypriortotrip.

Page|26

OTHER:

Attachexplanationorusebackofform.Thissectionmaybeusedforbusinesstelephonecalls,

faxes,postage,baggagetips,etc.

TOTALEXPENSESTOBEREIMBURSED:

Sumofexpensestobereimbursed.

ENTERTAINMENT:

Attachitemizedreceiptandonreversesideofreceiptlistwhowasentertainedandbusiness

purposeofentertainment.Thefundholder’sinitialsmustappearbelowthefundnumber.

LESSTRAVELADVANCELOANRECEIVED:

Entertraveladvanceloanreceived.

TOTALDUETRAVELER/UNCG:

CalculateamountduetotravelerorUNCG.Reconcileanyamountduetothetravelerorthe

University.ShowamountsduetheUniversityinparenthesesandattachacheckinthatamount

totheTRV‐1.ChecksshouldbemadepayabletoUNCG.Donotsendcash.

TRAVELER’SSIGNATURE:

Traveler’ssignaturestatingthatexpenseslistedareaccurateandwereincurredforUniversity

business.

SUPERVISOR’S/DEAN’SSIGNATURE(S):

Signatureofsupervisoroftravelerstatingthatthereimbursementrequestisjust,necessary

andreasonableandincompliancewithUniversitypolicies.

FUNDNUMBERS:

Listfundstocharge.

FUNDHOLDERINITIALS:

Ifthefundholderissomeoneotherthanthepersonauthorizingthetravelreimbursement,

thenthoseapprovalsforanyfundslistedmustbeobtainedseparatelyunder‘FundInitials’.

AMOUNTREIMBURSED:

Fillinthetotaldollaramounttobechargedtothesix‐digitfundnumber.Thetotalofthe

‘ReimbursableAmounts’columnmustequalthetotalinthe‘TotalExpensestobeReimbursed’

box.

COMMENTS:

Addanyadditionalcomments,ifnecessary,toprocesstravelauthorization.

TRV‐1FORMCOMPLETEDBY:

Printnameandtelephonenumberofindividualcompletingtravelauthorization.

Page|27

FormTRV‐1,TravelAuthorization/ExpenseReport

FrequentlyAskedQuestions

Q.Doestravelpolicyapplytonon‐employees,suchasstudents?

A.Asper5.7oftheStateBudgetManual,“non‐stateemployeestravelingonofficialstate

businesswhoseexpensesarepaidbythestatearesubjecttotheseregulations,including

statutorysubsistenceallowances,tothesameextentasareStateemployees.”Please

rememberthatasper3.4.1oftheStateBudgetManual,TrustFundsarenotexemptfrom

budgetmanualtravelpolicies.

References

OSBMBudgetManual

NorthCarolinaGeneralStatutes

InternalRevenueService